Embracing Disruption

Premium brands, smaller waists: GLP-1s and the premiumization of healthcare

GLP-1–based anti-obesity medicines are incretin therapies that reduce appetite and improve cardiometabolic risk, shifting obesity treatment from short courses toward chronic medical management. The competitive set has broadened from Novo Nordisk’s semaglutide franchise (Wegovy) to Eli Lilly’s tirzepatide (Zepbound), which the FDA approved for chronic weight management in adults with obesity or overweight plus comorbidity.

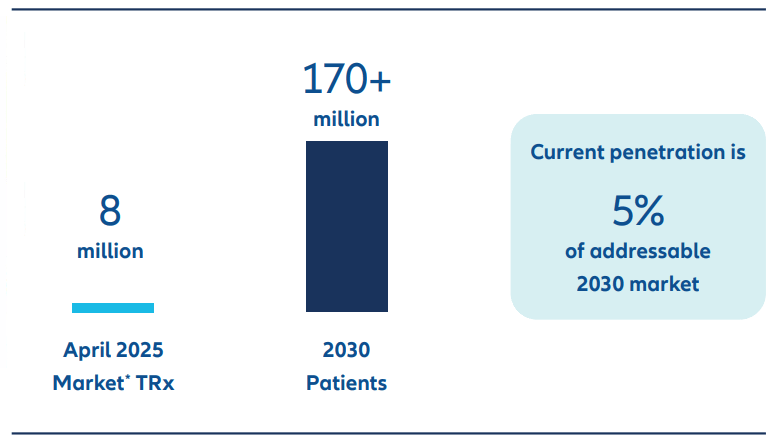

The global obesity drug market is projected to reach USD 100 billion in 2030, with the GLP-1 injection market alone expected to increase five-fold from 2024 to 2030, reaching USD 81 billion. With the weight-loss bar already at 20%-plus, greater emphasis is likely to be placed on improving tolerability and the quality of weight loss, with nonincretin mechanisms, such as amylin, in focus. GLP-1s are set to remain a backbone treatment of obesity.1 Furthermore, current penetration is still in its very early days – in the US (the largest obesity market), it is still only at 5% of addressable 2030 market.2

Exhibit 1: US market penetration vs projected market size

Eli Lilly “2025 LILLY ADA INVESTOR EVENT“; 22/07/2025. *US Incretin Analog Market: IQVIA weekly NPA total prescriptions for injectable GLP-1s, oral GLP-1s and GLP-1/GIP dual agonist.

In the most recent wave of developments, Novo secured an FDA label expansion for Wegovy for cardiovascular risk reduction (a key step toward medicalizing reimbursement beyond “cosmetic” weight loss) and, importantly for “premiumization,” also announced approval of a once-daily oral Wegovy option – potentially widening adoption among injectionaverse patients while intensifying competition in convenience-led segments. Meanwhile, Lilly has reported positive Phase 3 topline results for its oral GLP-1 candidate Orforglipron in obesity, underscoring that the next battleground is likely to be pill-based scale-up, access, and brand-led persistence rather than efficacy alone.

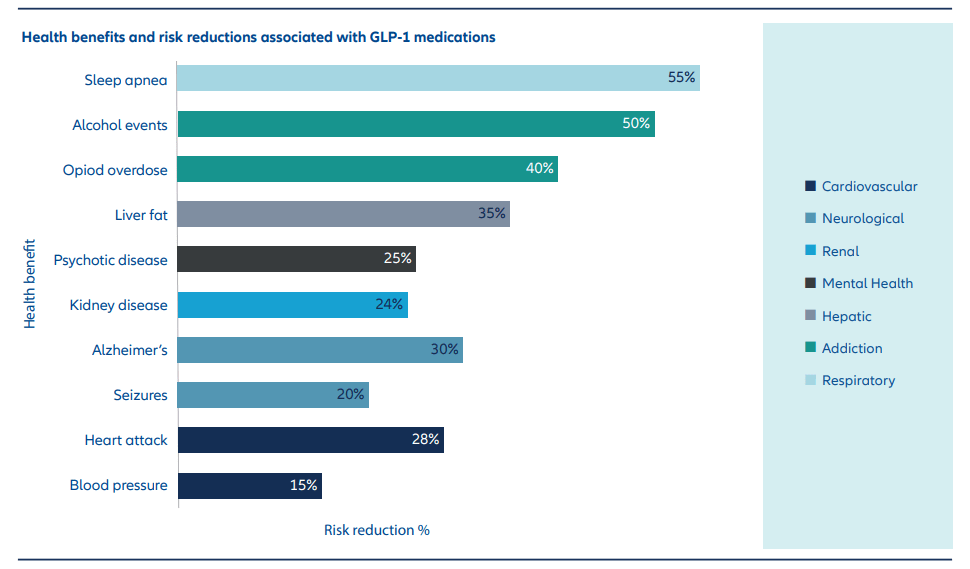

Exhibit 2: GLP-1 health benefits and risk reduction

Source: “Comprehensive Analysis of GLP-1 Medications Health Benefits (<www.glp-1tribe.com>, Weight Loss Efficacy, Side Effects, Safety, and Population Health Impacts”; Study data from https://investor.lilly.com/; https://www.appliedclinicaltrialsonline.com/.

Weight-loss pharmacotherapy increasingly a discretionary wellness purchase

Demand for anti-obesity drugs is developing in a “consumer-meetschronic-disease” pattern: very high clinical efficacy (often ~10–20% weight loss for newer GLP-1/GIP agents) has expanded interest well beyond specialty obesity clinics into primary care and direct-toconsumer channels, while the addressable population is massive (ICER notes >40% of U.S. adults have obesity – over 100m potential users). As demand collides with coverage constraints, a growing out-of-pocket/cash-pay segment is emerging, where consumers effectively treat weight-loss pharmacotherapy as a discretionary wellness purchase: manufacturers and intermediaries are explicitly building self-pay pathways (e.g., LillyDirect’s self-pay programme; cash pricing/discounting for Novo’s oral Wegovy via large pharmacy networks), reinforcing “premium brand” dynamics. This overlays a broader cultural shift – McKinsey’s research frames a large and resilient global wellness market (≈ USD 2T) and notes consumers, especially younger cohorts, continue prioritizing wellness spending even amid trade-down behavior – creating fertile ground for premium-priced health solutions where perceived value is high.3

As payer coverage for clinically obese patients with comorbidities is expected to broaden across multiple global markets4, access should gradually improve and generate richer real-world evidence base on outcomes and safety. Over time, this expanding dataset is likely to increase awareness and confidence in the therapies, helping to address residual concerns around side effects. If that trust builds, demand could extend beyond strictly medical use into a larger “aesthetic” or lifestyle-adjacent segment – effectively shifting parts of the category from traditional pharma into consumer-oriented wellness and materially expanding the total addressable market.

Duopoly-like market

The global pharmaceutical weight-loss market has effectively consolidated into a duopoly, led by Novo Nordisk and Eli Lilly. Together, the two companies command the vast majority of demand for next-generation obesity treatments, shaping both pricing dynamics and the pace of market expansion.

This market structure is underpinned by high barriers to entry. The development of effective weight-loss therapies requires lengthy clinical trials, significant capital investment, and the capacity to manufacture at scale for global distribution. Regulatory approval processes and reimbursement negotiations further entrench the position of established players, making meaningful near-term disruption from smaller competitors unlikely.

Within this environment, both companies are investing heavily in expanding manufacturing capacity and advancing next-generation formulations.

For investors, the resulting duopoly offers an attractive combination of strong pricing power, high earnings visibility, and long-term growth potential. Competitive pressures remain limited in the medium term, allowing leading players to focus on scaling production and extending product lifecycles.

A material impact across various sectors

From an investor perspective, the growing adoption of weight-loss drugs – particularly GLP-1 therapies – could have a material impact across a wide range of sectors and industries, creating both winners and losers. While parts of the healthcare ecosystem are likely to benefit, other industries face meaningful structural risks as consumption patterns evolve.

In healthcare, a sustained decline in obesity rates could reduce the longterm incidence of chronic conditions such as diabetes and cardiovascular disease. Over time, this may lower overall healthcare system costs. At the same time, demand for preventative care, diagnostics, and ongoing health monitoring could increase as consumers place greater emphasis on long-term wellbeing rather than acute treatment. Companies involved in drug delivery technologies – such as manufacturers of injection pens, auto-injectors, and related devices – as well as pharmaceutical distributors, may also benefit from higher volumes and recurring demand.

Beyond healthcare, several adjacent industries stand to gain. Weight loss associated with GLP-1 therapies is often accompanied by muscle loss, which is expected to drive higher demand for protein-rich foods and nutritional products. Companies with strong positioning in high-protein foods and supplements could see their total addressable market expand meaningfully. In contrast, segments focused on ultra-processed foods, snacks, and calorie-dense products may face shrinking volumes and increased pricing pressure. GLP-1 drugs significantly alter consumer behavior. Users of these drugs consume 15-40% fewer calories compared to placebo groups and exhibit reduced cravings for sweet, salty, fatty and alcoholic foods, leading to notable changes in dietary patterns.5

The restaurant industry is also likely to feel second-order effects. Consumers using weight-loss drugs tend to have reduced appetite and may dine out less frequently. Restaurants that fail to adapt could underperform peers that adjust to changing consumer preferences. Alcohol consumption may decline as well, adding to existing demand headwinds already evident across parts of the beer and spirits industry.

Within consumer discretionary, gyms and fitness studios could benefit as individuals who have lost weight increase physical activity to rebuild muscle mass and improve fitness.

Out-of-pocket costs of antiobesity pills: USD 149 to 299/ month – the cash price for Novo Nordisk’s Wegovy pill, depending on the dose.

Similarly, demand for sporting goods and athletic apparel may rise alongside higher participation in exercise and outdoor activities.

Investors should take these thematic developments into account, as they have the potential to reshape consumer behavior and materially influence portfolio allocation decisions.

AI-enabled drug discovery could revolutionize R&D

A rising cadence of large pharma–AI platform collaborations (e.g., Lilly– Nimbus for AI-driven oral metabolic candidates; Boehringer–Variant Bio for AI/genetics discovery) and early clinical proof points from AI-discovered programs suggest AI could become a tangible catalyst for faster, differentiated pipelines. In subsequent papers, we will explore AI-enabled drug discovery in more depth as an emerging and increasingly investable theme – examining the key catalysts and evidence base that could translate scientific progress into durable value creation.

Sources:

1 Bloomberg Intelligence, “BI Disease Overview: Obesity”; 21/08/2025.

2 Eli Lilly “2025 LILLY ADA INVESTOR EVENT“; 22/07/2025.

3 McKinsey & Company; “The $2 trillion global wellness market gets a millennial and Gen Z glow-up“ 29/05/2025.

4 Medicare coverage for GLP-1 drugs for obesity will begin in spring 2026, starting with a pilot program that could become mandatory in 2027. Within this channel, the US government will secure Novo Nordisk’s Wegovy and Eli Lilly’s Zepbound at a per-patient cost of $245 per month, with beneficiaries paying a $50 co-pay to access these medications. Source: Bloomberg Intelligence and centers of Medicare & Medicaid Services.

5 Source: https://www.rolandberger.com/en/Insights/Publications/GLP-1-Fad-or-future.html.