Agility counts in a year of disruption and divergence

Going into 2022, investors will want to prepare their portfolios for bouts of volatility and lingering inflation, likely by diversifying more broadly across asset classes, styles and regions. But they should also take this opportunity to factor in the disruptive structural trends that are driving – and even upending – our expectations of the future.

Economic growth seems likely to decelerate after the “base effect” rebound we saw in 2021. Covid-related uncertainty and supply bottlenecks will likely prove to be a drag on growth, as well as a continued source of price volatility. There should also be a divergence in growth figures and central bank support in various parts of the world, and the markets will likely react quickly to any positive or negative macroeconomic data. All the while, inflation seems likely to stay higher than many market-watchers expect.

So what does this mean for investors’ portfolios?

We invite you to explore three structural themes that are likely to play a key role in the coming year.

Navigating Rates

Investors need to watch the speed of interest rate adjustments, fluctuating exchange rates and shifting inflation expectations. We think central banks and many investors underestimate the probability that consumer price inflation may turn out higher than expected – and last longer than is currently priced into financial markets. While some central banks have already imposed rate hikes, and others are close behind, they are also likely to remain “behind the curve” in responding to inflationary pressures. So while inflation may creep up, we don’t expect to see an end to the decades-long era of overall low rates – which means investors must find new ways to protect purchasing power and search for yield.

Navigating rates: reinforce portfolios against monetary policy mistakes

Central banks are in uncharted territory in terms of the monetary stimulus they’ve been providing. This raises the risk of central banks making a policy mistake that would upend parts of the global economy, make inflation more volatile and affect financial markets. As a result, central banks are walking a fine line.

Consider that the US Federal Reserve (Fed) and European Central Bank (ECB) have announced plans to scale back their asset purchase programmes and hike rates. At the same time, these and other central banks won’t want to “tighten” too much. They have become more comfortable with higher inflation and are allowing it to outpace their rate increases. In monetary policy-speak, they are “behind the curve”. Given today’s high private and public sector debt levels, they are also aware that if they were to pull back on the monetary reins too hard, they could risk triggering defaults.

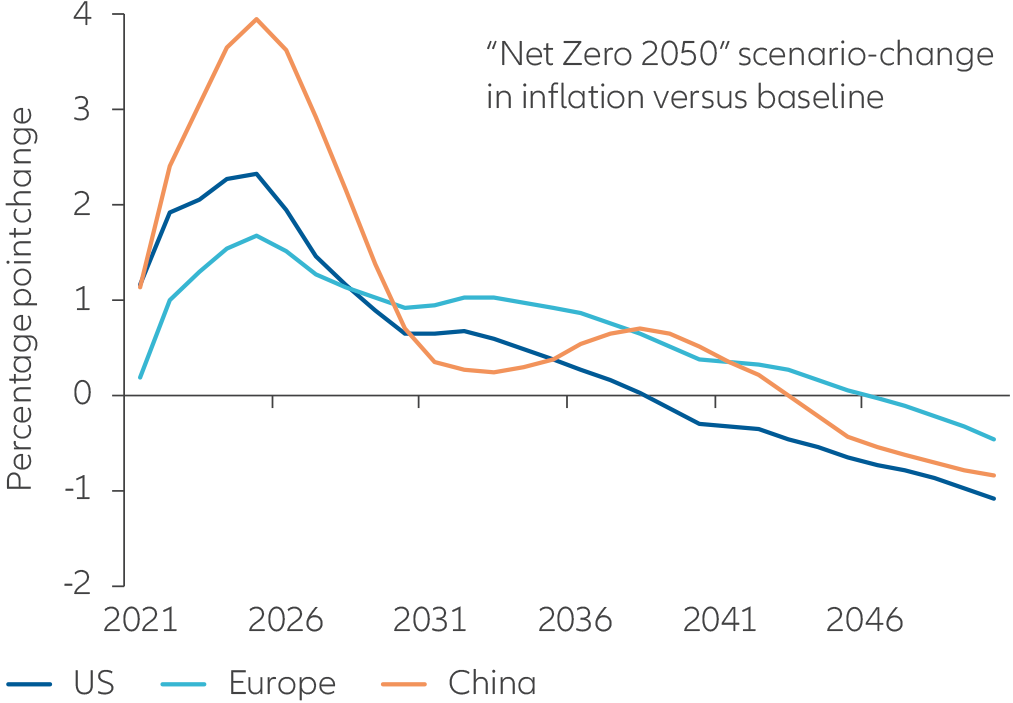

This continued monetary support is one reason we expect higher inflation to last longer than the markets currently expect. And there are other long-term developments in the real economy that are at least marginally inflationary: slowing international trade, higher labour compensation and the fight against climate change are just a few. Rising prices for CO2 certificates and the economic adjustments needed for a “green” economy will likely increase prices initially, even though they should benefit economic growth and the planet over the long term (see climate change chart).

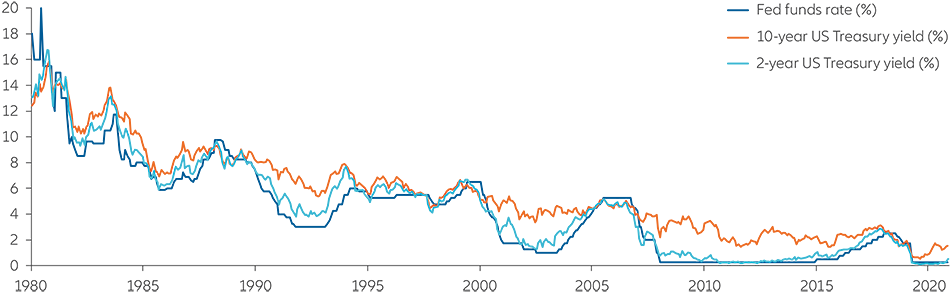

But overall, the forces that have driven interest rates steadily towards zero over the past four decades are still at work, and we believe they will remain dominant for some time (see rates vs yields chart). Against this background, rates and yields seem likely to stay lower for longer overall.

The fight against climate change may push up near-term inflation

US, EU, China: change in inflation vs baseline for “net zero 2050” scenario

Source: Network for Greening the Financial System. Data as at June 2021.

Rates and yields have dropped for decades

Fed funds rate and US Treasury yields (1980-2021)

Source: Refinitiv Datastream, Bloomberg, Allianz Global Investors. Data as at June 2021.

What it means for investors: consider fundamental changes for this fast-changing environment

Given our view that interest rates are likely to stay lower for longer – while inflation remains higher than it was in the pre-Covid era – investors may want to rethink their asset allocations. Different approaches will likely be needed to navigate diverging levels of growth and yield potential. And it will be critical to be far more agile to navigate an era when market conditions can shift quickly – and the potential for policy mistakes remains elevated. Here are four ideas for the year ahead:

-

Use “barbells”

Higher central bank interest rates, reduced bond purchases and higher inflation will likely lead to weaker bond prices and rising yields. One way to approach this is to view portfolios as “barbells” that span two groups of assets: those suited to preserving capital (including government bonds, credit, cash-like investments and liquid alternatives) and those designed to generate capital growth and income (including emerging-market bonds, stocks and even private-markets assets). Investors can target a variety of outcomes via multi-asset solutions that combine elements from each group.

-

Think themes

Thematic investing offers the ability to diversify portfolios while aligning with powerful, long-term social and demographic shifts. Themes such as healthcare transformation and the embrace of digital technologies represent new sources of growth and yield potential – which traditional classifications by sector or region may miss. The UN Sustainable Development Goals provide a helpful “window into the future” to identify companies that are addressing these opportunities.

-

Tap private markets

Private markets may hold particular interest for institutional investors in this environment, where illiquidity premia are holding up well. They can offer various built-in hedges if the recent rise in inflation becomes a longer-term trend. Investors can also use private markets to seek financial alpha while also improving the world in which we live. This is particularly timely given the public and private sectors’ commitment to “build back better” in the wake of the Covid-19 pandemic – for example, by investing in education, healthcare or enhanced digital infrastructure.

-

Stay agile

Monetary and fiscal support is still high, though fading. Growth and inflation data will likely remain much more volatile than in past cycles, making predictions harder to make. And growth may be increasingly driven by “endogenous” (internal) factors such as consumption or high-tech advancement. In such an environment, scenarios can change quickly. That means the optimum mix of assets will naturally need to shift in response – all while keeping exposure to riskier assets without taking on undue levels of overall risk. This calls for a highly dynamic, active approach that can switch positions rapidly as economic conditions evolve.

Appreciating China

The world’s second-largest economy is in the midst of an unparalleled strategic transformation, and it’s important not to lose sight of that even as economic growth slows and regulatory clampdowns impact certain sectors. Volatility will continue to be a hallmark of investing in China, but we remain convinced of the long-term investment case. Those who understand China’s wider political context and strategy – and navigate its markets actively – may be best-placed to avoid bumps in the road along the way.

Appreciating China: don’t be deterred by volatility

A critical factor to watch in 2022 is how much China – the world’s second-largest economy – will continue to unnerve markets. Growth has undoubtedly slowed, and recent regulatory issues have triggered market selloffs. But in our view, these changes are part and parcel of investing in China, and investors should seek to weather them over the long term. More immediately, there is plenty of good news out of China. Its banking sector is robust, its government is committed to strengthening its “seat at the table” in the global economy and the country is financed to only a small extent from abroad. China’s equity market valuations are generally cheaper than their US counterparts. And with the nation preparing for the 20th Party Congress in October 2022, government officials will likely do what they can to boost optimism.

Make no mistake: investors will encounter rough spots. At the core of US-China tensions is an ongoing “digital Darwinism” – a multi-decade global power race fuelled by technology and artificial intelligence. In response, China is looking to boost self-sufficiency – promoting high-tech manufacturing and domestic consumer spending to help reduce dependence on foreign trade. “National champions” are set to emerge – companies that provide home-grown alternatives to previously imported goods and drive China’s global competitive advantage.

What it means for investors: understanding China’s history and strategy is critical

When it comes to China, we believe active management is essential – both to navigate this environment and to use the inevitable volatility to build positions. We see opportunities in sectors linked to China’s strategic need for self-sufficiency (semiconductors and robotics) and stocks linked to China’s carbon-emissions targets (renewable energy and the electric vehicle supply chain). Investors could consider adding thematic “satellite” investments to their core China A-share allocations, focused on big-potential areas such as healthcare or technology.

The road won’t always be smooth, and investors would be well-served by accepting that volatility has historically accompanied China’s stockmarket growth. It also helps to understand China’s economic, social and cultural history and how its policy agenda is evolving. Complementing bottom-up analysis with an understanding of the broader context can help investors discover where the country’s strategic priorities translate into opportunities.

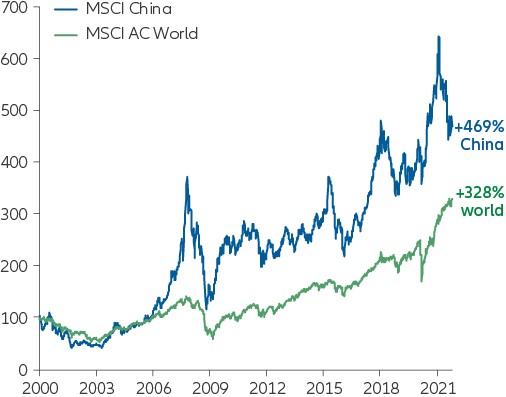

China equities have exhibited higher volatility – and attractive returns

MSCI China and MSCI ACWI performance since 2000 (in USD, indexed to 100)

Source: Bloomberg, Allianz Global Investors. Data as at October 2021. Based on net total return performance in USD. Past performance is not indicative of future results.

Achieving Sustainability

With the global effort to reach “net-zero” emissions within a few decades, how can investors use their portfolios to have a positive impact? Investor demand, fast-evolving regulations and a deluge of data will raise the bar on what impact investors can achieve – and how they can achieve it. It’s a highly complex topic, involving disparate stakeholders at different stages of their net-zero journeys. We expect sustainability to be a disruptor for the older economy, as citizens around the world look to have a smaller ecological footprint while having a broader environmental and social “handprint”.

Achieving sustainability: invest in a global shift in mindset

In 2022, we expect to see sustainability increasingly factored into every investment decision – from mitigating future risks to finding today’s solutions. Here are five ways in which sustainable investing could help set the global economic agenda for the year ahead.

-

Defining net-zero pathways

In the wake of the latest UN Climate Change Conference (COP26), there will be increasing scrutiny on the “pathways” that individual stakeholders must follow to reach net-zero carbon emissions. Individual countries must articulate where they currently stand and how they plan to change, and all stakeholders will need to converge on a common goal. Their decisions will change how goods are manufactured and consumed, which will affect economic growth.

-

Processing data and navigating conflicts

We expect new regulations to have a significant effect on how businesses operate. Investors will need more resources to process enormous amounts of data, and they may see environmental, social and governance (ESG) factors compete with one another. For example, moving away from fossil fuels may benefit the environment, but eliminating certain jobs may limit access to food or healthcare – hence the need to facilitate a “just transition” to clean energy. Investors will need support to navigate a critical, complex and fast-evolving landscape.

-

Making sustainability structural

A new economy is taking shape, and sustainability affects every company, sector and region. For example, the “just in time” mindset that focused on the lowest cost and highest efficiency has been exposed by the Covid-19 pandemic. Supply chains have broken down and need to be rethought, and true costs that were once externalised and delayed may now be reflected upfront in the prices consumers pay.

-

Focusing on impact

Emphasising ESG factors can help improve the resilience of businesses and systems, but the pandemic and escalation of destructive weather events are shifting the agenda. Investors increasingly want their capital to effect real-world change. The growing field of impact investing offers an answer by providing a credible and scalable pathway to balancing a targeted, measurable environmental or social impact on the one hand, with a financial return on the other.

-

Moving beyond climate

Think of sustainability in three interlinked areas. The focus on climate change determines the temperature in which future generations will live. But we also must learn how to sustain life in that temperature, which means navigating planetary boundaries that respect biodiversity and provide a safe operating space for humanity. And all these changes must be made in a way that improves equality and social welfare, which is why inclusive capitalism will become increasingly critical.

What it means for investors: broaden your thinking and focus on impact

Don’t relegate sustainable investing to one portion of a portfolio. It is increasingly integral to a successful investment strategy. Consider, for example, how sustainability crosses over to our two other primary investment themes for 2022:

- China has a huge role to play as the world seeks to reach net zero and implement energy solutions, so it’s critical for the rest of the world to understand China’s journey – and engage with it.

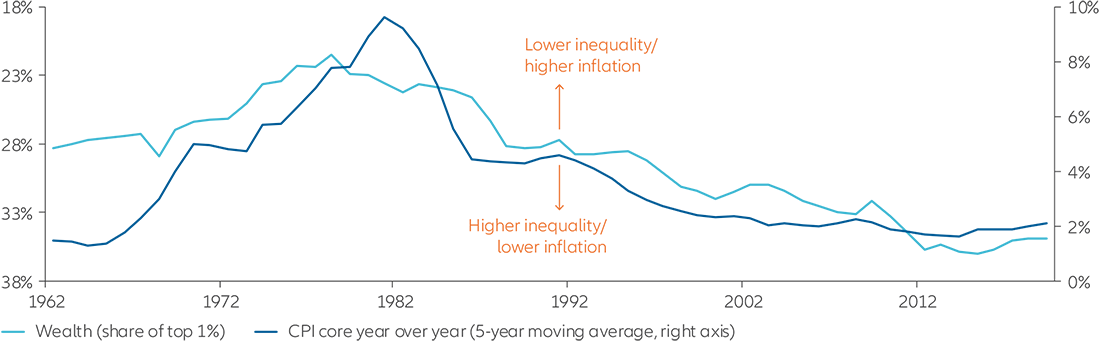

- The “greening” of the economy will likely add to inflationary pressures in the medium term – even as inequality falls (see chart). Meanwhile, green investments may be able to provide the attractive yield potential that will be vital in today’s low-interest-rate environment.

As the world addresses these critical issues, we expect to see a broader notion of “impact” come to the fore – including how companies are managing their ecological footprint in addition to their broader social handprint. Investors should rightly push for this expanded view of business success. Moreover, meeting these critical sustainability goals will require large amounts of financing, which is why we expect all asset classes (including public and private) in all regions to be increasingly aligned with impact investing.

If future economic inequality falls, inflation could move higher

US wealth inequality vs consumer inflation

Source: World Inequality Database, Bloomberg. Data as at 2019.

-

Volatile markets may provide fertile ground for stockpickers

From a macroeconomic perspective, there are at least three questions to consider as 2022 unfolds. As these questions are answered, the equity markets will likely be volatile, which can be fertile ground for stockpickers:

- What will be the evolution of real interest rates given the potential economic slowdown and the cyclical upward pressure on inflation?

- As China's growth continues to decelerate, what support measures will the government put in place to cushion the slowdown? And how will the trade relationship of China and the US evolve in the context of “digital Darwinism”?

- How will countries work together on a range of big issues? The energy transition is critical: how will we calibrate the long-term transition to green energy and the shorter-term impact of the recent economic rebound on the oil supply and energy markets? In terms of the global pandemic, how will improved access to the Covid-19 vaccine limit the unpredictability of virus waves and lockdowns, and will this lift global economic growth beyond the “base effect”?

As equity investors, we will be particularly attuned in 2022 to the effort to combat climate change. There will be a growing number of initiatives from investors, asset managers, governments and communities, and all of them will need to be factored into investment decisions. This is where the integration of strong ESG data can make a big difference. Above all, it will be important for equity investors to be highly selective. At the same time, they must remain focused on their established investment processes and risk controls.

-

Amid low yields, look for proactive central banks and “green” bonds

While the global economy is set to remain in expansionary territory in 2022, we recognise that the initial impressive economic growth rates achieved as economies reopened following the Covid lockdowns will not be sustained. Central bank and government action since the onset of the pandemic has significantly reduced some of the worst-case scenarios for the global economy, and dramatically diminished the prospects of a credit crunch. The path of inflation over the next 12 months will have to be watched closely, along with the way central banks react to these pressures.

Given that multiple factors indicate that interest rates will stay lower for even longer, rethinking portfolios to account for this outlook should be an urgent priority for investors. Risk management and diversification strategies must become far more agile. We are looking closely at selectively overweighting bonds from emerging-market countries where central banks have been proactive in addressing inflation risks – as long as valuations look attractive. In addition, global issuance of green, social and sustainability-linked (GSS) bonds recently hit a record high – evidence of fixed-income investors growing increasingly serious about tackling climate risks and social challenges.

-

Address low rates, high valuations and inflation with multi-asset strategies

Growth and inflation data will likely remain much more volatile than in past cycles, making predictions increasingly hard to make. That is why we will pay particularly close attention to the potential for negative shocks, such as the risk of a new Covid-19 variant. But overall, we continue to hold a cautiously optimistic view for 2022.

Equities and other risk assets should be partially supported by the tail end of the post-Covid global recovery, and by cash-rich investors fighting off the effects of negative real (after-inflation) rates. Traditional fixed income may be somewhat challenged, as inflation risks stay elevated and major central banks reduce their government-bond purchases. As investors seek diversification against inflation risk, they may want to use a combination of commodities, liquid alternatives and inflation-linked bonds. Overall, the current environment of low to negative interest rates, high valuations and higher inflation might prove challenging for traditional asset classes. Multi-asset strategies that offer exposure to a broad set of asset classes – and have the flexibility to take long and short positions – may help investors address a wider range of risks.

-

2022 may offer a favourable backdrop for private markets

Given the wide amount of uncertainty inherent in the macroeconomic outlook for 2022, institutional investors should consider the diversifying effect of private markets – which in the main have limited correlation to public markets. From private equity to private debt, from renewable infrastructure to development finance, private markets can cover a wide range of investment scenarios. And with the ability of some private-markets strategies to deploy over a multi-year time horizon, investors can aim to further enhance their overall diversification.

Investors may want to pay particular attention to these areas in 2022:

- Growing geopolitical tensions (particularly between the US and China) seem likely to help certain countries (such as Vietnam and India) benefit from a reorganisation of supply chains. Private-credit strategies focused on the Asia-Pacific region may be well-positioned in such an environment.

- The urgency of responding to climate change has triggered an acceleration of concrete opportunities in energy-transition transactions – particularly infrastructure investments accessed through the private markets. This marks a tremendous and swift paradigm shift.

- No matter your view on inflation, it can likely be accommodated through infrastructure investments. For investors with long-term horizons, infrastructure equity provides a robust solution. And for investors seeking to navigate potential interest-rate increases while yields are near historic lows, the high-yielding infrastructure credit space can offer attractive floating rates and even short durations.

-

Emphasise sustainability while looking “beyond climate”

As the year progresses, we will likely have answers to several critical questions around sustainability and its impact on the economy:

- Will COP-26 prove to be a defining moment for net zero, how will countries finance and fulfil their pledges, and how will their decisions affect economic growth?

- What could be the near and longer-term implications of the climate transition on inflation and the affordability of goods?

- What surprises can we expect from increased scrutiny of the modern economic value chain, and can reporting practices coalesce around clear standards?

The answers to these questions will add to the growing amount of data that investors need to embed into their decisions, and it’s not yet clear whether this will be helpful or a hindrance. Moreover, as sustainability becomes an increasingly essential factor in asset allocations, we may see more volatility and divergence in market performance – which will be yet another input for investors to process. This foots back to what will make 2022 an important year for impact investing. As investors push for positive societal outcomes related to climate and beyond, there will be a deluge of data on how those outcomes are scoped, measured and reported. Making this information actionable will be a challenge, but one that will ultimately facilitate positive change for the planet.

Read more from us

-

MSCI All Country World Index (ACWI) is an unmanaged index designed to represent performance of large- and mid-cap stocks across 23 developed and 24 emerging markets. MSCI China Index is an unmanaged index that captures large- and mid-cap representation across approximately 85% of the China equity universe. Investors cannot invest directly in an index.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Equities have tended to be volatile, and do not offer a fixed rate of return. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bond prices will normally decline as interest rates rise. The impact may be greater with longer-duration bonds. Credit risk reflects the issuer’s ability to make timely payments of interest or principal—the lower the rating, the higher the risk of default. Emerging markets may be more volatile, less liquid, less transparent, and subject to less oversight, and values may fluctuate with currency exchange rates. Investments in alternative assets presents the opportunity for significant losses including losses which exceed the initial amount invested. Some investments in alternative assets have experienced periods of extreme volatility and in general, are not suitable for all investors. Environmental, Social and Governance (ESG) strategies consider factors beyond traditional financial information to select securities or eliminate exposure which could result in relative investment performance deviating from other strategies or broad market benchmarks. Past performance is not indicative of future performance.

This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP (Australian Registered Body Number 160 464 200) is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

1916457