Active is: Sharing insights

Will Fed easing support risk assets?

Summary

An insurance easing cycle looks likely in the second half of 2019. This has historically meant positive returns for equities, but we still favour a defensive position across risk markets.

Key takeaways

|

The Fed’s next move will be policy easing

At the Federal Open Market Committee’s (FOMC’s) June meeting, Fed chair Jerome Powell and team delivered a dovish message that exceeded market expectations, signalling that the Fed is ready and willing to step in with policy easing “as appropriate.” Several updates to its statement, economic projections and press conference suggest the Fed’s next move will be a rate cut.

In particular:

- The FOMC statement dispensed with its previous “patient” language, while economic activity was recategorised as “moderate” and uncertainties about the global outlook “increased.”

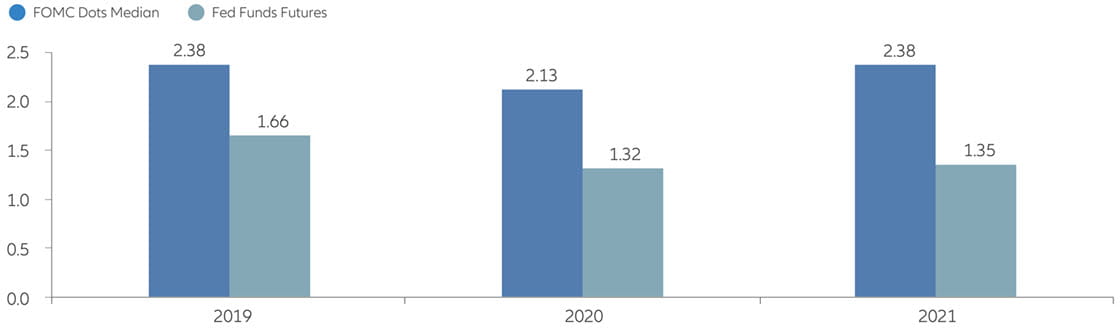

- The FOMC’s updated median “dot plot” showed a rate cut for 2020, instead of the rate hike it showed at the last meeting (Exhibit 1). Notably, seven of the 17 FOMC members projected 50 basis points of easing this year.

- Powell indicated clearly in the press conference that he “will act as appropriate” in terms of the Fed’s rate path, noting “many participants now see the case for somewhat more accommodative policy.”

Exhibit 1: Fed dot plot vs. market expectation

Source: Bloomberg, July 2019

Our base case now calls for a 25 basis point rate cut in both September and December. We believe a Fed easing cycle is likely to commence in the second half of 2019. We could see a rate cut as early as July – despite a solid jobs report this month – if the Fed chooses to undertake insurance cuts, particularly in light of rising levels of negative-yielding debt globally and the ongoing inversion of the US yield curve.1

Additionally, while we see the Fed most likely moving in 25 basis point increments, a 50 basis point rate cut during this cycle is not out of the question, depending on whether data deteriorate swiftly.

Not all easing cycles are created equal: “insurance” vs. “pre-recession” easing

What would a Fed easing cycle mean for risk assets broadly? We observed data around the past eight Fed rate-cutting cycles – from 1981 to 2007– and highlight several key takeaways.

Two types of Fed easing cycles

We categorise Fed easing cycles into two broad groups: insurance cycles or pre-recession cycles. Insurance cycles are those where the Fed eases while the economy is not in a recession, but economic headwinds loom. Pre-recession cycles are when the Fed eases as the economy is entering – or already in – a recession. Of the last eight easing cycles since 1981, the split between insurance and pre-recession cycles was even, with four in each camp (Exhibit 2).

Exhibit 2: Insurance and pre-recession Fed easing cycles since 1981

| Fed Funds target rate % |

||||||

|---|---|---|---|---|---|---|

| Start | End | Days | Start | End | Change | Type of cut |

| 6/1/1981 | 12/15/1982 | 562 | 20.00 | 8.50 | -11.50 | Pre-recession |

| 10/2/1984 | 8/19/1986 | 686 | 11.75 | 5.88 | -5.88 | Insurance |

| 10/19/1987 | 2/10/1988 | 114 | 7.25 | 6.50 | -0.75 | Insurance |

| 6/5/1989 | 9/4/1992 | 1187 | 9.75 | 3.00 | -6.75 | Pre-recession |

| 7/6/1995 | 1/31/1996 | 209 | 6.00 | 5.25 | -0.75 | Insurance |

| 9/29/1998 | 11/17/1998 | 49 | 5.50 | 4.75 | -0.75 | Insurance |

| 1/3/2001 | 6/25/2003 | 903 | 6.50 | 1.00 | -5.50 | Pre-recession |

| 9/18/2007 | 12/16/2008 | 455 | 5.25 | 0.25 | -5.00 | Pre-recession |

| Average | 521 | -4.61 | ||||

Source: Allianz Global Investors Global Economics & Strategy, June 2019.

Risk returns in insurance vs. pre-recession cycles

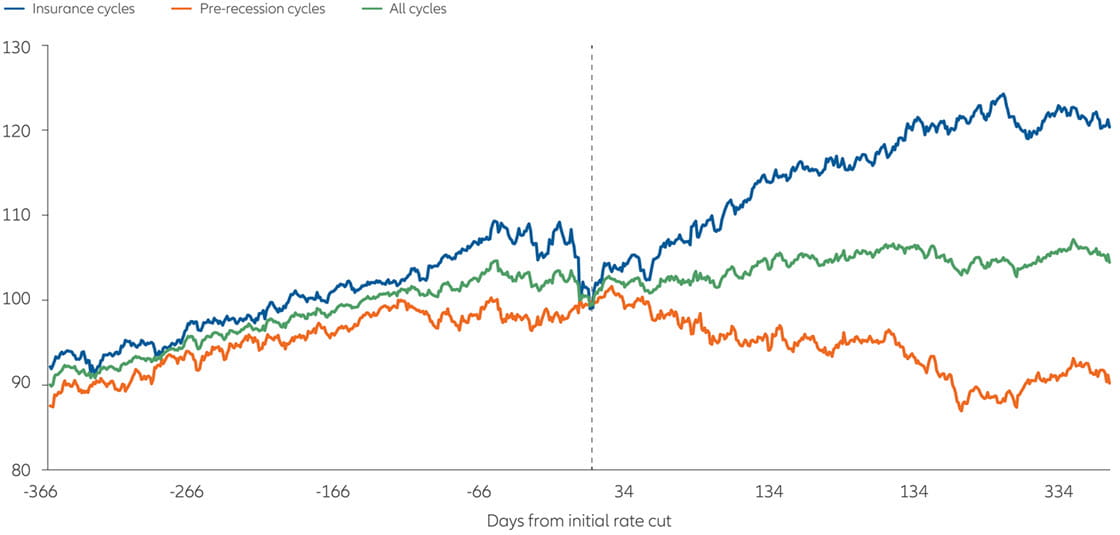

Historically, market performance has varied significantly between insurance and pre-recession cycles. One year into an easing cycle, the S&P 500 generated a 20.4% average return during insurance cycles compared with a -10.2% average return during pre-recession cycles (Exhibit 3). This divergence suggests that where we are in the US economic cycle may dictate how risk assets respond to the next round of Fed easing.

Exhibit 3: S&P 500 performance one year before and after initial rate cut

Source: Factset, June 2019. Past performance is no guarantee of future results.It is not possible to invest directly in an index.

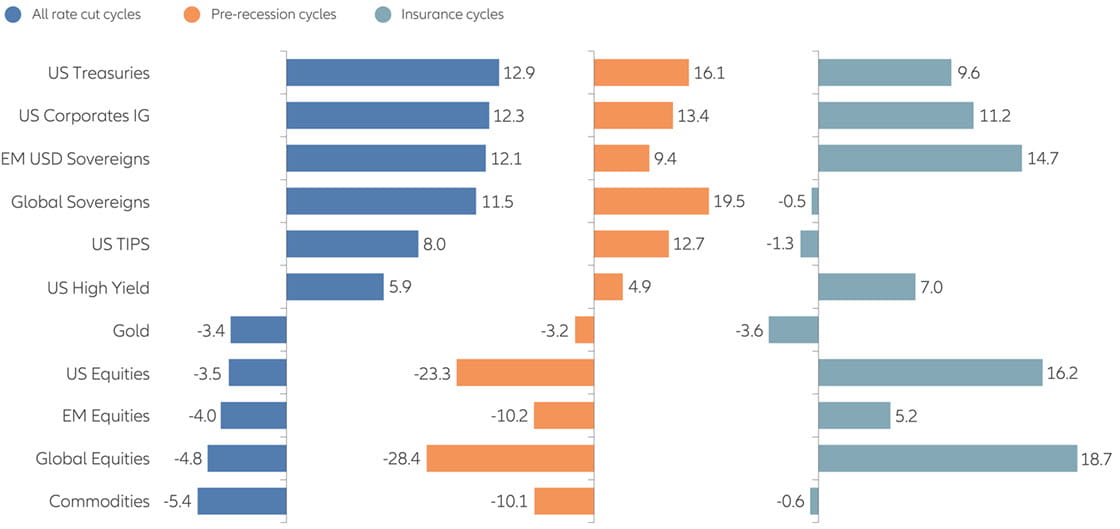

The reason for this divergence between easing cycles lies primarily with equities: the US, global and emerging market equities all performed substantially better in insurance cycles than in pre-recession cycles (Exhibit 4). Certain asset classes performed similarly regardless of cycle type. Fixed-income assets generally performed well in both insurance and pre-recession cycles, while real assets, such as gold and commodities, tended to underperform regardless of the cycle type.

Exhibit 4: Excess return vs cash during Fed rate cut cycles

Source: Allianz Global Investors Global Economics & Strategy, Bloomberg, Datastream, June 2019

From a sector perspective, we find that cyclical sectors – such as technology, industrials and consumer discretionary – tend to perform well in insurance cycles, while more defensive areas like healthcare and consumer staples lag. The reverse is generally true during pre-recession easing cycles: cyclical sectors tend to underperform, although we also see more defensive sectors like utilities lag materially (Exhibit 5).

Exhibit 5: S&P 500 GICS sector performance one year after initial rate cut

| Insurance cycles | Pre-recession cycles | Differential | |

|---|---|---|---|

| Technology | 39.9% | -21.8% | 61.7% |

| Health Care | 14.7% | -10.4% | 25.2% |

| Energy | 16.5% | -11.4% | 27.9% |

| Financials | 18.3% | -30.1% | 48.4% |

| Cons Discr | 20.3% | -13.4% | 33.6% |

| Materials | 6.0% | -3.6% | 9.6% |

| Industrials | 23.7% | -14.8% | 38.5% |

| Cons Staples | 11.0% | -0.9% | 11.9% |

| Comm | 25.3% | -25.2% | 50.5% |

| Utilities | 0.6% | -21.2% | 21.8% |

Source: Factset, June 2019. Past performance is no guarantee of future results.It is not possible to invest directly in an index.

An “insurance” Fed easing cycle could be likely this time

The US economy – alongside the global economy – is certainly decelerating, but growth isn’t expected to turn negative. While we believe fragility in the economy has increased, and tail risks from areas like trade and geopolitics remain, we do not yet see an imminent recession risk over the next six months, when the Fed is expected to begin its easing cycle.

Real growth forecasts in the US are expected to slow – from 3% in 2018 to just above 2% this year, and to below 2% in 2020. Indicators such as manufacturing purchasing managers’ indices (PMIs) and OECD leading indicators are also weakening, while the S&P 500’s earnings growth is likely to slow to the low single-digits this year, down from 20% last year.

However, we continue to see one key area of overall strength in the economy: the US consumer, which is critical, considering domestic consumption comprises nearly 70% of US GDP.

Unemployment remains at near historic lows, at 3.7%, while consumer confidence remains near its multi-year high, despite recent volatility. We have also seen a recent rising trend in consumer spending, particularly among discretionary categories; lower rates may also provide support to critical areas like housing and auto sales. The recent tariff truce between President Trump and China’s President Xi at the G20 meeting in Japan was incrementally positive, particularly for the US consumer, as both sides agreed to resume trade discussions “on the basis of equality and mutual respect.”

Importantly, the US also decided to postpone tariffs indefinitely on the final USD 300 billion of Chinese imports, which mainly targeted consumer goods, such as textiles, apparel and footwear. While global trade tensions continue to remain an overhang, the immediate threat of another round of consumer-focused tariffs is off the table for now.

The 1990s case study: similarities to today

As the Fed likely embarks on rate cuts later this year, we see somewhat similar economic conditions to those that previously resulted in two insurance easing cycles during the 1990s.

In 1995, the Fed trimmed rates as an insurance measure when inflationary pressures eased; inflation (core CPI) fell from 5% the previous year to the 2%–3% range, while unemployment fell from 5.6% to 4.0%. Today, the US economy has a similar inflationary and unemployment profile, with core CPI stagnating in the 2% range and unemployment falling to multi-decade lows.

In 1998, the Fed enacted another insurance cut on the economy, reducing rates pre-emptively to cushion the effects of an external shock – namely the Asian financial crisis – which could have potentially hindered US growth. Today, concerns about worsening US-China trade relations and escalating tariffs could be considered a similar external threat, acting as a potential catalyst for a slowdown; the Fed could respond to these potential shocks with insurance cuts.

Portfolio positioning: remain defensive and up-in-quality

While the Fed may be embarking on the start of an insurance easing cycle, which has historically been favourable for risk assets, it is worth noting that market returns in the first half of the year were already remarkably strong – with the S&P 500 up nearly 18%.

Given that insurance easing cycles historically result in positive returns, we believe active exposure is still necessary, with a focus on defensive and up-in-quality assets across risk markets.

- We continue to favour a barbell approach in both domestic and global equities. In the US, we like select cyclical sectors that have done well historically in insurance easing cycles, including areas of technology with secular growth themes, such as mobile payments, cloud, and cybersecurity. On the other side of the barbell, we favour more defensive sectors like aerospace/defence, REITs2 and staples, which have all lagged technology this year but tend to perform well in a decelerating growth environment. Globally, we continue to prefer US equities from a developed market perspective, and also favour select Asian and emerging market equities.

- In fixed income, we continue to prefer an “up-in-quality” positioning in both US investment grade and high yield. Given the ongoing “hunt for income” that investors face in today’s low-rate environment, we also see select opportunities in European and Asian high yield, especially for US-dollar-denominated investors. In addition, we continue to favour convertible bonds, which also offer the potential for equity upside.

- We remain overweight alternatives, both liquid and illiquid, which tend to be less correlated to both equities and fixed income, providing an appealing source of diversification. We believe areas like absolute return and long/short strategies, as well as private credit or infrastructure debt and equity, remain favourable at this stage of the cycle.

1) Source: Bloomberg, July 2019. Refers to the 3-month/10-year US Treasury yield curve.

2) Source: Real estate investment trusts.

898270

Want to view more?

Active is: Navigating geopolitics

UK: still no reason for optimism?

Summary

“Under-owned, cheap and unloved” – those words sum up how many investors view the UK today. Some see a fresh start in the arrival of a new prime minister eager to change the narrative. But it’s difficult at this stage to look beyond Brexit to make a convincing short-term investment case for UK assets, despite a number of enduring positive fundamentals.

Key takeaways

|

-

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is for Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations and is for information purpose only. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; in HK, by Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; in Singapore, by Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; in Japan, by Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424], Member of Japan Investment Advisers Association, the Investment Trust Association, Japan and Type II Financial Instruments Firms Association; in Taiwan, by Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan; and in Indonesia, by PT. Allianz Global Investors Asset Management Indonesia licensed by Indonesia Financial Services Authority (OJK).