Don’t downsize your goals

Two bond market ideas to help guard against rising inflation

Summary

After many years of falling inflation, the second half of 2021 could be remembered as the time when prices started to rise again. How should bond market investors respond? Here are two more ideas.

Key takeaways

|

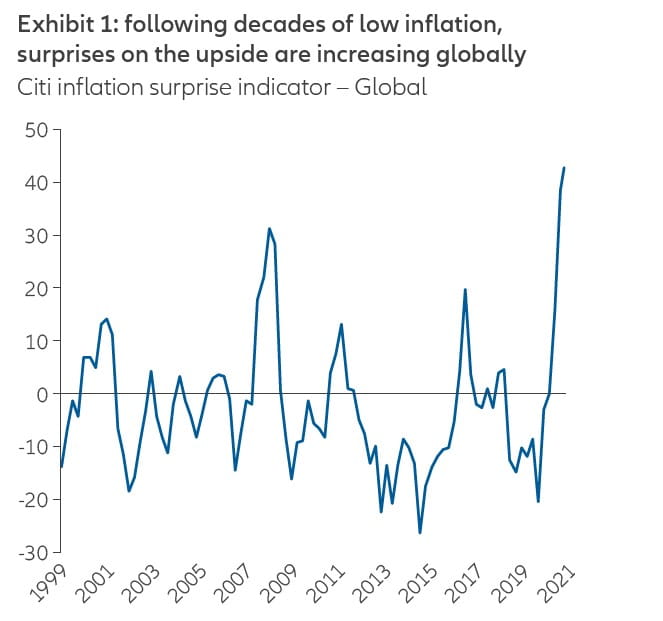

2021 could be remembered as the year that inflation returned. For decades inflation has stayed low globally, but in the last months of 2021, markets have experienced hotter-than-expected inflation and inflation surprises globally are at their highest level in over 20 years (see Exhibit 1).

Source: Bloomberg.

Is inflation structural or temporary?

The coronavirus pandemic with all its consequences – like the shutdown of manufacturing production in early 2020 – brought inflation to such low levels that even comparison with the first months of 2021 shows significant variations. This is the “base effect”, which tends to decrease over the following months as the terms of comparison become more homogeneous.

The essential question for financial markets is whether temporary factors or structural forces have been more significant in sparking inflation’s return. Temporary factors are certainly at play. They include the rising price of key raw materials, primarily oil; the strong recovery of economic growth that leads to effects known as output gaps – where the actual output of the economy may exceed its potential output; and supply disruptions.

But our economists believe that financial markets may be underestimating the risk of higher inflation in the medium term. The consensus view considers the current rise in inflation to be a transitory phenomenon: a view the Federal Reserve, European Central Bank and other central banks firmly support.

In our view, there are good reasons to think that structural forces – factors that are permanent or sustained – could lead to stubbornly higher inflation. Changes in the labour market, especially as globalisation reverses, are pushing up the prices of goods and services. And, above all, the expansionary monetary policy of the US Federal Reserve and the European Central Bank, with their adoption of flexible inflation targets, implies they may be “behind the curve” – and interest rates could fail to keep pace with inflation.

That said, it is difficult to predict with certainty whether the increase in inflation will be structural or more temporary, as the long-term consequences of the pandemic are still not clear. While we clearly do not expect inflation rates to return to the levels seen in the 1970s, we believe that medium-term inflation risks are higher than currently anticipated by the market. We expect inflation premiums to rise slightly and inflation volatility to increase.

Two bond market options for inflationary times

Should higher inflation prove to be structural, there are two options worth considering when investing in the bond markets.

1. Inflation-linked bonds

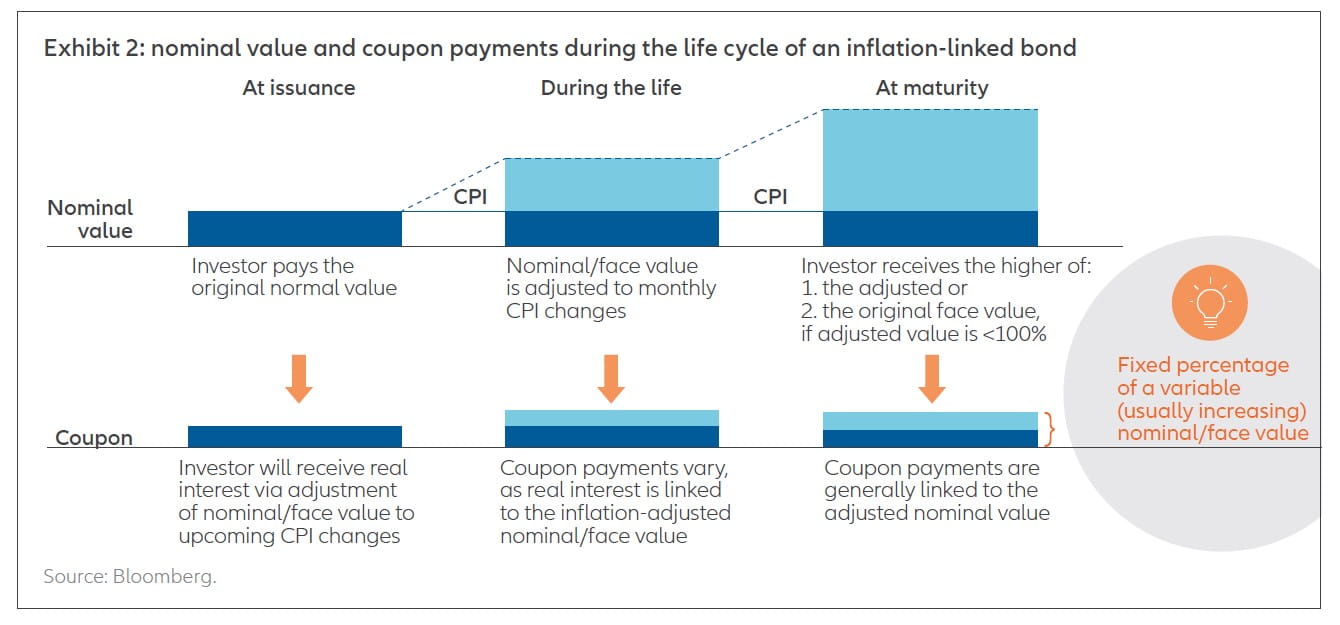

Inflation-linked bonds (ILBs) are designed to protect investors from inflation as the instruments benefit from rising inflation expectations. Because their principal and interest payments are contractually linked to a recognised inflation measure such as the US Consumer Price Index (CPI) or Europe’s Harmonised Index of Consumer Prices (HICP), rising prices translate directly into higher coupon rates and principal values. Exhibit 2 illustrates how principals and coupon values change, from issuance to maturity.

When to buy ILBs?

To assess the relative attractiveness of ILBs (also known as “linkers”) against nominal government bonds, we refer to the so-called break-even inflation rate, which is the difference between nominal yields and real yields. In other words, it indicates the inflation expectations priced into the market, or the rate differential at which holding a nominal bond and an ILB of the same issuer and the same maturity would be equivalent.

Therefore, if we expected inflation to be higher over the life of the bond than the break-even rate, we would earn a higher return holding ILBs, while at the same time having lower inflation risk. The opposite would be true if we expected inflation to be lower than the break-even rate.

This means that the best market environment for investing in ILBs is when inflation is rising and markets are pricing higher inflation in the future, as they are today. This explicit link to changes in inflation makes ILBs an effective way to incorporate real returns into a portfolio.

A prolonged period of declining prices, or deflation, would be a less suitable market context for investing in ILBs because the principle and coupon payments would be based on the deflationary scenario. However, to mitigate this risk, more and more ILBs are issued with a deflation floor. This guarantees that the bond’s principal amount will not fall below par at maturity, so only the coupons are affected by the decline in prices.

As with any other bonds, ILBs are affected by interest rate risk, or duration. Interest rate risk could prove topical if real yields move higher following a shift by central banks to a more restrictive monetary policy, as ILBs usually have long durations. To mitigate this, portfolio managers can deploy swaps to isolate and manage the pure inflation risk.

2. Floating rate notes

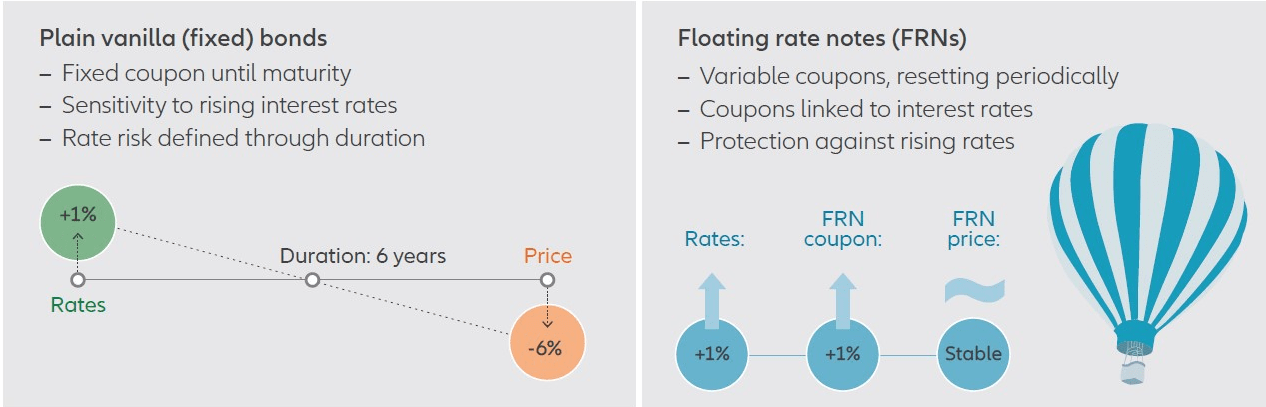

Another area of the bond market that can outperform in inflationary environments is floating rate notes (FRNs), which have their coupons linked to a specified base rate. Floating rate coupons normally adjust around every three months: as the cashflows reset in line with interest rates, the bond price tends to remain stable around par.

An everyday example could be a mortgage with monthly payments that adjust in line with a central bank’s official rate. On the other side of the equation, banks and corporations issue bonds with coupons typically tied to a short-term market interest rate such as LIBOR (London Interbank Offered Rate), or the newer interbank indices including SOFR (Secured Overnight Financing Rate) in the US and SONIA (Sterling Overnight Indexed Average) in the UK.

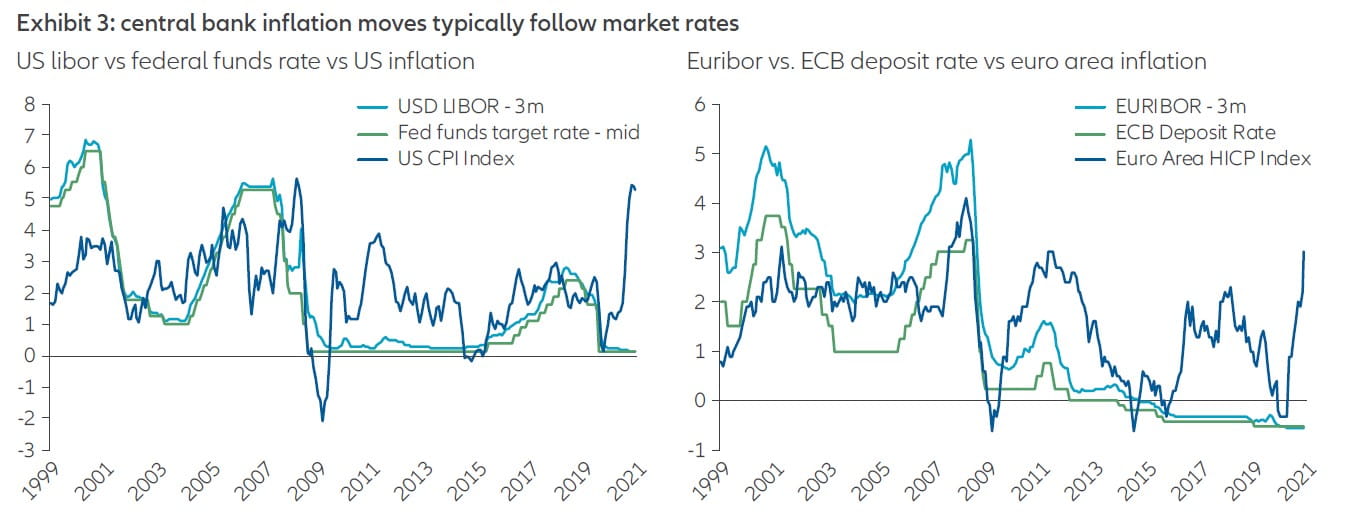

One potential benefit of linking floating rate bonds to market-determined rates is that they tend to be responsive to inflation risks. By contrast, central bank policy often lags through inertia or a deliberate desire to support growth and employment. Exhibit 3 shows that the market rate often (though not always) moves first and further than the official central bank rate in response to changes in inflation. Investors, therefore, benefit from price stability in floating rate bonds, while gaining additional income if inflation and short-term market rates do rise.

Source: Bloomberg.

The floating rate coupon’s premium over and above the base rate is known as the discount margin; it reflects the riskiness of the issuer and the bond itself. This margin ranges from a handful of basis points for a highly rated issue backed by prime collateral, to several percent for lower quality corporate bonds.

FRNs therefore contain credit risk, in contrast to ILBs which are generally government-issued. Also, to simplify a little, FRN performance can be driven more by market views on short-term inflation, while ILBs reflect the longer-term expectations of break-even rates.

As such, the performance of FRNs is linked to the business cycle and investor sentiment. Individual issues may be subject to credit downgrades or even defaults in the worst-case scenario. Conversely, when economic growth and corporate results are strong, discount margins will shrink and FRNs will perform well.

Thinking about the different economic scenarios presenting themselves, FRNs tend to perform poorly in times of deflation and contracting growth – the first quarter of 2020 being a prime example. Strong growth coupled with rising inflation and short-term market rates is the best environment for FRNs, as was the case in 2004-6 or 2017-18. Stagflation – high inflation coinciding with a slowdown in economic growth – would present a mixed bag; rising rates would benefit FRNs as coupons adjusted upwards, however only higher rated and defensive issuers would perform well. More cyclical and sub-investment grade companies typically require growth to sustain their debts.

It should be noted that FRNs may reduce, but not completely eliminate, interest rate risk, as there can be a lag of a few months before the coupons reset.

In the asset/mortgage-backed sector, the bonds are typically secured by specific collateral or assets of the issuer (so that holders of the debt, such as the fund, have a priority claim on those assets in the event of the issuer's default or bankruptcy). The value of collateral may be insufficient to meet the issuer's obligations, and the fund's access to collateral may be limited by bankruptcy or other insolvency laws. Our investment techniques, analyses, and judgments may not produce the outcome we intend.

A long-term plan to counter inflation

Inflation is one of the most harmful forces that fixed-income investors face, as it erodes bonds’ real returns. Consequently, a long-term investment strategy should consider protection against the risk of inflation.

ILBs do not only offer a natural hedge against a rise in inflation, they are also an efficient tool for investors seeking diversification within a broader fixed income portfolio, as they tend to be less correlated to other forms of fixed income. Our expertise at Allianz Global Investors covers not only ILBs, but also a wide range of performance drivers linked to inflation, such as inflation swaps, break-even trades and active management of duration and curve positioning.

Likewise, FRNs can benefit portfolios at times of rising inflation and rising short-term rates, even if central banks choose to let the economy “run hot”. Active management is also called for here, however, given the possibility of credit risk.

To return to the current macroeconomic environment, higher inflation is back. And while consensus opinion still regards the drivers of inflation as transitory, we think it will be higher than many market-watchers expect. For this reason, it may well be time for investors to seek safeguards.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP (Australian Registered Body Number 160 464 200) is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

1876714

Want to view more?

Active is: Expanding the boundaries of investing

Nine themes for investing in China’s transformation

Summary

As China’s economy quickly transforms itself, a thematic approach based on structural macro trends is an effective way to identify the winners.

Key takeaways

|