Look for active opportunities following the Fed’s hawkish move

Summary

The US Federal Reserve has raised its benchmark interest rate against a backdrop of high inflation and concerns about the geopolitical situation stemming from events in Ukraine. While markets have previously taken rate-hike cycles in their stride, this time could be different, as the Fed seems to be more hawkish than initially expected. Investors should actively seek out relative-return opportunities.

Key takeaways

|

What’s happened

At its 15-16 March meeting, the US Federal Open Market Committee (FOMC) raised the federal funds target rate by 25 basis points, bringing the target range to 0.25%-0.50%. This is expected to be the first in a series of hikes that could take short-term interest rates above the neutral rate of 2.4%. (The median “dot plot” projections of participants indicate a fed funds rate of 2.8% by the end of 2023.) The Federal Reserve’s focus is on rising inflation, higher energy prices and a tight labour market as it attempts to keep the US economy from overheating and prevent a de-anchoring of long-term inflation expectations. But the US central bank is taking nothing for granted: it has said it “will be prepared to adjust the stance of monetary policy ... if risks emerge”.

What it means

The Fed’s monetary policy has been exceptionally accommodative for years and, by not raising rates fast enough to stay ahead of inflation, the Fed has fallen significantly “behind the curve”. Yet this rate-hike cycle is starting amid the most challenging environment of any cycle kick-off since the mid-1980s:

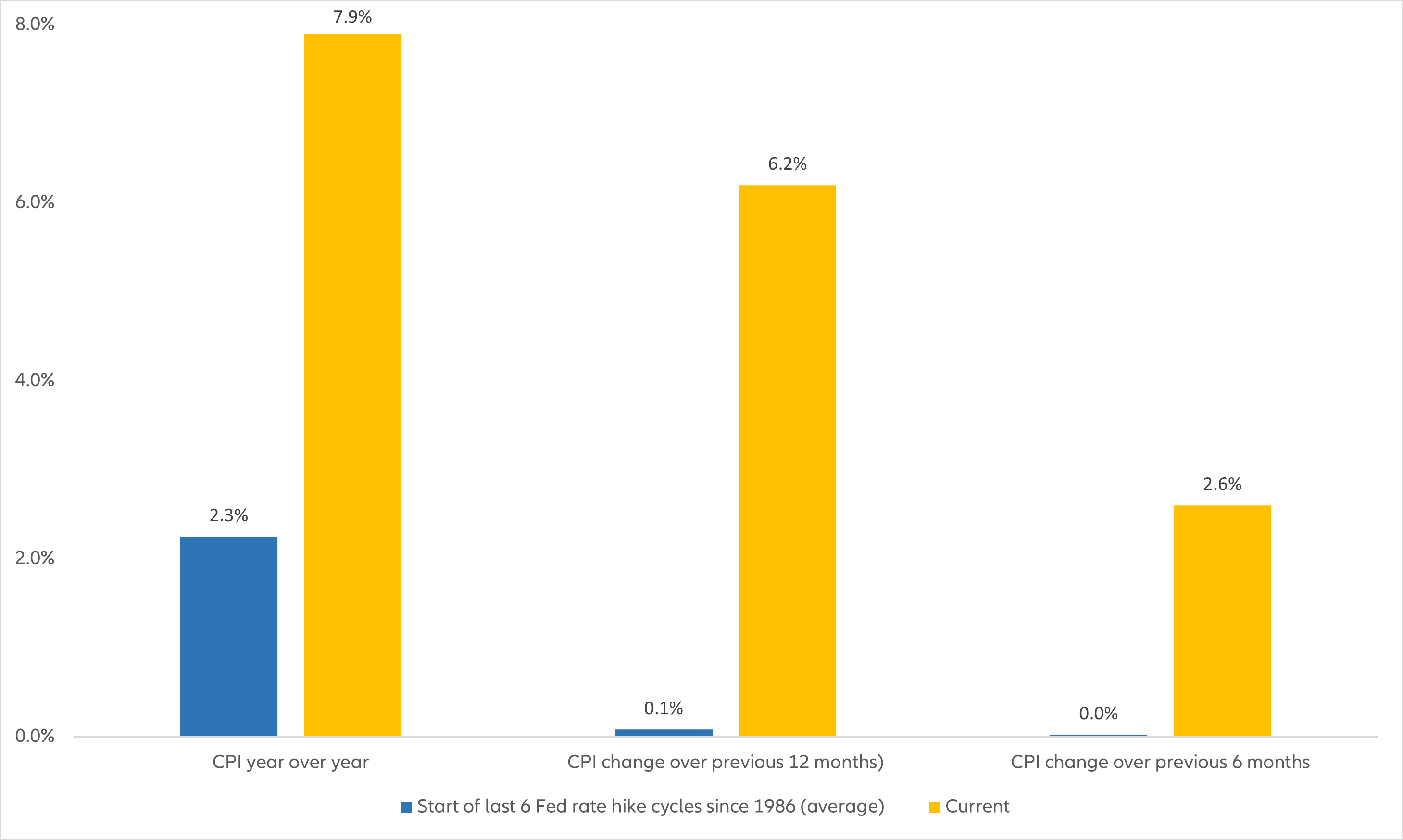

- CPI is at a 40-year high: 7.9% now* vs an average of 2.3% at the start of the six Fed rate-hike cycles since 1986.

- The unemployment rate is at 3.8% now vs 5.7%.

- The output gap is already positive, while it has previously been, on average, negative.

- Today’s long-term real interest rates are at a deeply negative level, compared with positive real rates in all six previous cycles since 1986.

With its inflation-fighting credentials at stake, the Fed has no choice but to embark on a long journey towards a tighter policy stance. Central banks cannot afford to take a lenient stance on inflation – even against the current backdrop of rising geopolitical risks (which, in the Fed’s view, “create additional upward pressure on inflation and weigh on economic activity”), low visibility and slowing economic growth. Moreover, the latest spike in energy and commodity prices represents a supply shock on top of already high inflation rates, and it is likely to weigh on real incomes and dampen economic activity.

When implementing the necessary monetary tightening to tackle upside inflation risks, the Fed aims for a “soft landing” of the US economy. But when looking back at history, the odds for such an outcome appear rather slim. Four of the last five rate-hike cycles in the US were ultimately followed by a recession. Our base-case view, which seems confirmed by the Fed’s 16 March statement, is for a steady tightening of monetary policy by the Fed until broader financial conditions have reached a sufficiently restrictive level to tackle medium-term upside risks to inflation. This process might be disrupted, however, if financial stability or recession risks escalate along the way.

What investors should do

Consider the US and UK over the euro zone

The Fed had done much to prepare market participants for its latest rate decision, which explains the relatively muted equity-market reaction. Indeed, the evolution of the situation in Ukraine is more important for investors’ short-term risk appetite. The longer it takes to find a negotiated solution, the more uncertainty will persist around potential impacts on global inflation through supply-chain disruptions and rising energy and agricultural prices. This also explains why we continue to have a tactical preference for the US and UK over euro-zone equities, despite more attractive valuation levels for the latter. Investors will continue to favour the relatively “safer” US market in US dollars and the commodity-heavy UK market, while the euro zone’s growth and inflation prospects are more negatively impacted by higher energy prices.

Stay wary of the bond markets

Overall, an environment of moderately higher inflation tends to favour equities over bonds, even though inflation rates over 5%-6% historically penalise the equity market. The bond market could remain under pressure as it exhibits some unattractive risk premia, coupled with outflows indicating that investors are starting to question its diversification characteristics. The Fed is set to continue raising its leading interest rates – perhaps even above its neutral rate – while also soon moving to quantitative tightening “at a next meeting”. As such, we expect a further rise at the long end of the US yield curve, even though the immediate reaction should be for a flatter yield curve as the short end reacts more than the longer end. Yields in the euro zone are also set to rise, especially once the situation in Ukraine improves, since the European Central Bank is adhering strictly to its key target of maintaining inflation at 2%.

Adopt a granular view in credit

Do opportunities exist in the credit markets where spreads have widened recently? US high-yield bonds look the most promising area as yield differentials with government bonds have become attractive, especially if one expects only “slowflation” and not stagflation in the US. However, the view of our Multi Asset expert group is that it would take a reduction in volatility to spur us to re-enter the asset class – something we do not expect in the coming weeks. The same is true for emerging-market debt. Here, a granular view is vital: some countries will profit from higher energy prices while others could come under tremendous pressure. This is particularly true for countries already made fragile by the Covid-19 pandemic, thanks to the combination of a higher US dollar and spiking import and commodity prices (especially for agriculture goods) – a volatile mix that could lead to civil unrest.

Prioritise value

From a style perspective, this is certainly a market in which value – especially quality value – should continue to outperform growth. Historically, value has outperformed in environments of rising inflation, while the actual valuation differential strongly favours value versus growth.

Be more active on a relative basis in equities

On equities, our Multi Asset expert group maintains our “neutral minus” view in the short term, whereby we expect markets to move sideways with a risk to the downside. The more hawkish Fed action confirmed this view. We would therefore avoid “buying the dips” for the time being and instead become much more active on a relative basis. In the medium term, we have open questions with regards to the path of equity-market performance. True, markets have typically taken previous rate-hike cycles in their stride. But there have been exceptions, including extended periods when investors were unrewarded for taking market (beta) exposure. We continue to see risks of another such period with broad-based disappointing asset returns explained by:

- A low starting point for nominal/real interest rates and subdued risk premia in several asset classes.

- The risk that the Fed may condone a “reverse portfolio effect” to get prompt traction on broader financial conditions.

- Tightening into slower growth, which raises medium-term stagflation risks.

- Today’s geopolitical volatility causing underestimated, far-reaching economic and financial market repercussions.

US headline CPI is much higher this time around than it has been in previous rate-hike cycles

CPI: current vs average of previous 6 cycles (1986 to 2018)

Source: Bloomberg. Data as at 28 February 2022. Past performance is not indicative of future results. Dates of previous six Fed rate-hike cycles: 16 December 1986 to 04 September 1987; 29 March 1988 to 24 February 1989; 04 February 1994 to 01 February 1995; 30 June 1999 to 16 May 2000; 30 June 2004 to 29 June 2006; 16 December 2015 to 19 December 2018.

Key terms to know

- Behind the curve: term used to describe when central banks do not raise interest rates fast enough to head off inflation.

- CPI (consumer price index): usually refers to headline CPI, also known as headline inflation. This is a key inflation metric for the US and UK, among other regions. Refers to the full hypothetical “basket” of goods and services vs core CPI/core inflation. Because headline inflation is volatile, it is considered not very predictive over the short term.

- Fed funds target rate: the range of short-term interest rate at which banks lend to each other.

- Loose/easy monetary policy: economic shorthand for how central banks expand the supply of money (via low rates, asset purchases and more) to stimulate economic growth. Also known as expansionary or accommodative monetary policy. The inverse of “tight” monetary policy.

- Output gap: a measure of the amount of economic slack that can be absorbed without generating too much inflation.

- Quantitative easing: term used to describe central banks’ purchases of bonds and other securities – a process that is intended to suppress longer-term interest rates by driving up the prices of those securities (yields fall when prices rise). The opposite of quantitative tightening.

- Rate-hike cycle: period of time when the Fed (or other central banks) have raised short-term interest rates, measured from the first hike to the last.

- Real: after inflation is factored in (as in real yields, real growth rate, etc).

- Reverse portfolio effect: orderly upward shift of the entire risk premium curve.

- Risk premia: the four key risk premia for nominal government bonds are the real risk-free rate of return, the real term premium, the expected inflation rate and the inflation risk premium.

- Soft landing: used to describe how central banks raise interest rates just enough to slow economic growth without causing a recession.

- Stagflation: a period of high inflation, slow economic growth and high unemployment.

* Source: CPI data at 28 February 2022.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is for Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations and is for information purpose only. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; in HK, by Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; ; in Singapore, by Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; in Japan, by Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424], Member of Japan Investment Advisers Association, the Investment Trust Association, Japan and Type II Financial Instruments Firms Association; in Taiwan, by Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan; and in Indonesia, by PT. Allianz Global Investors Asset Management Indonesia licensed by Indonesia Financial Services Authority (OJK).

2082649

Want to view more?

Embracing Disruption

How do recent events in Europe affect the opportunities in transitional energy?

Summary

The invasion of Ukraine by Russian armed forces has destabilised security in Europe, creating a humanitarian crisis and market turmoil. With half of Europe’s oil and 30% to 40% of its gas imported from Russia, the invasion has escalated concerns over what Europe’s existing and long-term energy mix will look like in providing the region with dependable, affordable and climate-friendly access to energy. Here, we look at some considerations for investors assessing the energy market.

Key takeaways

|