Active is: Anticipating what’s ahead

At the mid-year point, dark clouds are forming in the US

Summary

As a companion piece to Neil Dwane’s global mid-year outlook, Mona Mahajan turns a spotlight on the US, where trade tensions and politics are weighing on markets. Given the increased uncertainty about the second half of the year, investors should stay active, defensive and diversified.

Key takeaways

|

After a strong start to the year, US-China trade wars hit the markets

On the heels of a near-20% decline in the S&P 500 Index at the end of 2018, the first four months of this year were met with market optimism. Investors took the opportunity to “buy the dip” amid an improving outlook on multiple fronts – in particular, the Federal Reserve’s pause in short-term rate hikes.

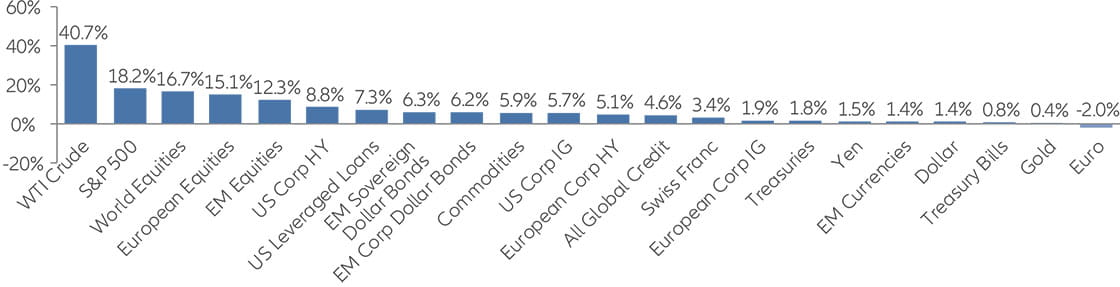

Many global risk assets showed strong returns in early 2019

Year-to-date total returns at the end of April

Source: FactSet. Data as at 30 April 2019.

But market performance and sentiment took a negative turn in early May, following escalating trade tensions between the US and China. President Donald Trump announced that the existing tariffs on USD 200 billion of Chinese goods would escalate from 10% to 25%, and the remaining USD 300 billion of Chinese imports not currently hit with tariffs could experience a 25% levy in the coming months.

Since this shift, the US-China trade relationship has notably deteriorated, with China indicating it is prepared for a long road ahead – and perhaps willing to start negotiations over again. A few key points are worth highlighting:

- US consumers are in the crosshairs. So far, consumer products have accounted for only 22% of the Chinese goods targeted by tariffs, but 60% of products targeted in the next wave of tariffs might be consumer goods. US consumers could feel an outsize impact, which may hurt confidence and potential growth.

- China only imports USD 125 billion of US goods, so they cannot retaliate in kind. Instead, China may utilize “non-tariff barriers” – including limiting US investments, adding additional regulatory hurdles, banning US products or brands, and ratcheting up geopolitical pressure where possible (eg, North Korea and Iran).

- Tariffs could be a long-term theme. Even if a trade deal is reached, the overhang of tariffs will likely remain – both as an enforcement mechanism and as part of President Trump’s trade strategy. In addition, given the recent hardening of rhetoric from China, the possibility of the US and China not reaching a deal has increased, in our view.

Trade war with Mexico averted – for now

In late May, President Trump threatened tariffs on Mexico, which could have escalated up to a 25% levy on all Mexican imports if the country didn’t comply with Mr Trump’s demands to enhance border security. But by early June, the US and Mexico reached an agreement, avoiding a major trade dispute.

Why did Mexico react so swiftly to the threat of tariffs? Relative to its economy, the US is a dominant trading partner, accounting for nearly 80% of all Mexican exports – or about 30% of its total GDP. By comparison, the US only accounts for 19% of Chinese exports, or 4% of its GDP. Mexico clearly had a bigger incentive than China to avoid tariffs with its largest trading partner.

Although the US seems to have achieved its goals in getting Mexico to enact changes, there may be repercussions for using tariffs to address non-trade issues. Mexico is a vital trading partner for the US, and this relationship has been strained. The potential passage of the new, post-NAFTA United States-Mexico-Canada Agreement (USMCA) has also grown less certain. In addition, China may be less inclined to strike a deal if it believes the US will implement new tariffs down the road based on non-trade-related policies.

Our outlook for growth and leading economic indicators

- If trade tensions escalate into a full-blown trade war, we see a downside to US and global real GDP growth. According to Bloomberg, an escalating trade war could shave 0.7 percentage points off of US GDP and 0.9 percentage points from China’s GDP, lowering global growth by 0.6 percentage points over the next two years.

- Given the trajectory of decelerating growth in the US, there is a growing risk that a trade shock could tip the economy into a downturn.

- While there are still pockets of bright spots in the US – notably a resilient US consumer supported by relatively low rates and low inflation – we see growing downside risks to economic growth, particularly if tariffs hurt consumer-goods pricing.

- Globally, we’ve seen substantial drops in key indicators such as purchasing managers index (PMI) data, which show economic trends in manufacturing. Together with declines in OECD leading indicators, this suggests potential softness in the global economy.

Our view on the second half is getting murkier

While the markets began the year with growing optimism for a second-half recovery, tensions between the US, China and Mexico have created concern – as has the decelerating momentum in leading economic indicators such as PMIs.

In the US, we think earnings expectations remain relatively elevated for the second half of the year, particularly in the fourth quarter. Consensus estimates call for a 7% year-over-year growth in S&P earnings. But if the US dollar continues to strengthen, US exporters could feel more pressure – a de-facto additional tariff as US companies try to sell their goods and services abroad.

With the growth outlook now deteriorating, markets have priced in two or three Fed rate cuts by year-end. In our view, the possibility of a rate cut has grown more likely to become reality given the potential for slowing economic fundamentals. However, we think the Fed will continue to be patient and data-dependent, and it won’t act unless data or expectations have meaningfully changed.

Overall, while we expect to see positive returns for the year, we don’t expect the pace of the first four months to continue. Geopolitical shifts could also increase volatility.

A mixed outlook for the remainder of 2019

| Indicator | 2017 | 2018 | 2019 expectation |

| US equities (S&P 500) | +19% | -6.2% | High single-digit to low double-digit |

| US rates (10-year yield %) | 2.41 (2.04 - 2.63 range) | 2.68 (2.41 - 3.24 range) | 2.25 - 2.75 |

| US real GDP growth | 2.2% | 2.9% | 2.4% (lower in full trade war) |

| US inflation (core PCE) | 1.6% | 2.0% | 2.0% - 2.2% |

| Fed rate hikes | 3 hikes | 4 hikes | 0 hikes (data dependent,

rate cut probability higher) |

| Volatility | All-time lows | Increases in spurts | Increases in spurts |

Source: Allianz Global Investors. Data as at May 2019.

Strategies for positioning portfolios

Given the increased uncertainty in the second half of this year, we advise investors to stay active, defensive and diversified.

- In both equities and fixed income, we suggest moving up in quality, favouring more defensive investments with stronger balance sheets and free-cash-flow metrics.

- In equities, consider a “barbell” approach: on one end could be tech firms specialising in mobile payments, cloud computing and cyber-security; on the other, defensive sectors such as health care, staples and defence/military positions.

- In terms of regions, we remain neutral on China, but favour parts of Asia that may benefit from supply chain disruptions (Thailand and Vietnam) or that recently completed positive election cycles (India and Indonesia). We are cautious on Europe, which has seen deteriorating growth and is more exposed to global trade declines.

- In fixed income, we are neutral on duration and favour higher-quality US investment-grade and high-yield issues. Parts of the securitised fixed-income segment could complement corporate bonds. We also see pockets of value in areas like European and Asian high yield.

- Additional alpha potential may be found in investments focused on ESG (environmental, social and governance) issues, infrastructure debt/equity strategies and absolute-return strategies. These asset classes could benefit as we head into the second half of 2019 and position for a maturing economic cycle.

Further reading

For a deeper dive into our global view, read:

In our mid-year outlook, trade and politics are top challenges

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Diversification does not ensure a profit or protect against a loss. Equities have tended to be volatile, and do not offer a fixed rate of return. Bond prices will normally decline as interest rates rise. The impact may be greater with longer-duration bonds. Foreign markets may be more volatile, less liquid, less transparent, and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations.

This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Panama, Peru, and Uruguay.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG, licensed by FINMA (www.finma.ch) for distribution and by OAKBV (Oberaufsichtskommission berufliche Vorsorge) for asset management related to occupational pensions in Switzerland; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

Want to view more?

Active is: Adapting to shifts in global trade

Do US-China trade tensions signal an end to globalisation?

Summary

It looks increasingly unlikely that the US and China will reach an amicable agreement to end their ongoing trade conflict. If tensions between the two countries continue to escalate, we could witness the end of a decades-long period of globalisation – with several major implications for investors.

Key takeaways

|

-

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is for Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations and is for information purpose only. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; in HK, by Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; in Singapore, by Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; in Japan, by Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424], Member of Japan Investment Advisers Association, the Investment Trust Association, Japan and Type II Financial Instruments Firms Association; in Taiwan, by Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan; and in Indonesia, by PT. Allianz Global Investors Asset Management Indonesia licensed by Indonesia Financial Services Authority (OJK).