Carbon offsets: debate to define role in net zero

Summary

Carbon offsets sparked fierce debate between policymakers and campaigners during COP26. Such discussion is vital to help fix some of the perceived flaws in a tool that will have a role to play in the net-zero drive.

Key takeaways

|

What are carbon offsets?

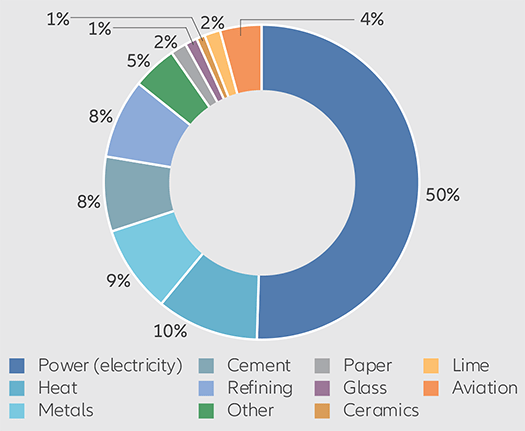

Carbon offsets allow an entity to compensate for its own carbon emissions with eliminated or avoided emissions from other activities or dedicated “carbon (offset) projects”. This compensation is made through carbon offset credits, with one credit relating to one metric tonne of carbon dioxide equivalent (CO2e)1 of emissions. Carbon offsets should not be mistaken for carbon credits, which are centralised tools for regulating the decarbonisation of high-emitting sectors. Granted by authorities, a carbon credit gives companies in certain sectors the right to emit greenhouses gases (GHGs). These credits can be traded to comply with set quotas. Today the best known and largest carbon market is the European Union Emissions Trading System (EU ETS), launched in 2005 and, which accounts for 90% of global carbon credits volumes and 40% of EU emissions (Exhibit 1). It is based on the “cap and trade” principle, a system for controlling carbon emissions. That said, carbon offset credits linked to emission-reducing projects – known as Certified Emission Reductions (CERs) – can also be traded on these regulated carbon markets. These are backed by UN guidelines and can be purchased by companies needing to comply with imposed carbon emissions caps. When a company voluntarily purchases carbon offsets to lower its net emissions, rather than to comply with mandatory emissions targets, these are called voluntary carbon offsets (VCOs).

Exhibit 1: Breakdown of 2020 EU ETS emission volumes by sector

Source: European Union Transaction Log, Bloomberg.

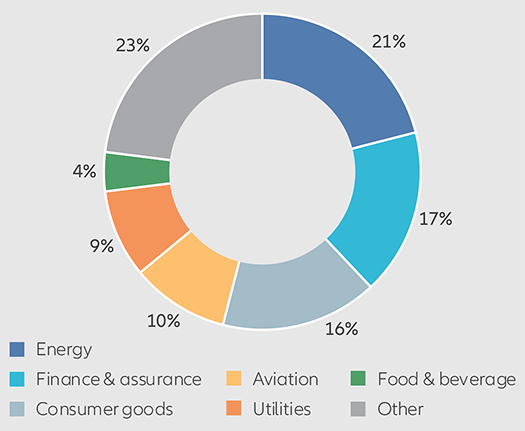

Exhibit 2: Breakdown of main European corporate buyers of VCOs by sector

Source: Forest Trends’ Ecosystem Marketplace Global Carbon Markets Data Intelligence & Analytics Dashboard, 2021. Washington, DC: Forest Trends Association. Based on purchased carbon offsets’ volumes.

The booming market in voluntary carbon offsets

Although the VCO market is still a fraction of the mandatory market in terms of traded carbon credit volumes, it is growing quickly. Many businesses that struggle to reduce emissions as quickly as they might wish or that find it tricky to outline a pathway to fully eliminate emissions are turning to VCOs to help. In 2020, the VCO and mandatory markets were worth approximately USD 500 million and USD 270 billion respectively.2 But the VCO market is expected to top USD 1 billion this year (representing approximately 300 million tonnes CO2e). This market would need to grow by at least 15 times by 2030 in order to be aligned with the 2015 Paris Agreement goal of limiting global warming to a 1.5°C rise by 2050.3

The pace of development in the whole ecosystem for VCOs is being driven by stakeholders across the value chain – from offset project developers to certifiers, brokers and final buyers. In many cases, VCOs direct private financing to climate-action projects that would otherwise struggle to gain financing. Unlike the mandatory market, VCO markets are not subject to regulation or international agreements and are accessible to all participants. The purchasers are mostly companies that wish to report lower net emissions (Exhibit 2).

What projects are used to generate voluntary carbon offsets?

Carbon projects can be broadly classified in two ways. The first is “purpose”, which includes projects that remove CO2 emissions directly from the atmosphere, as well as those that avoid emissions altogether. The second is “origin”, which includes nature or technology-based solutions. An example of a project that removes emissions through a nature-based solution is the Athna project in Alaska,4 which focuses on carbon capture through fighting deforestation. The project helps local communities to switch their source of income from selling trees to selling carbon credits from carbon-capture projects. Projects that tackle non-CO2 ozone-depleting substances such as refrigerant or aerosol gases are another example. These projects are qualified as an avoidance and technology-based solution.

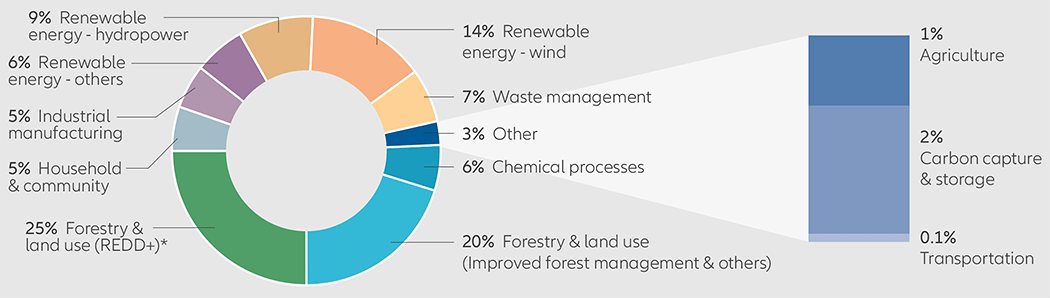

The level of investment for each project depends on its qualifications, with basic renewable energy projects at the lower cost end and the most technologically advanced carbon capture and storage (CCS) projects at the expensive end (Exhibit 3).

Exhibit 3: Voluntary carbon credits by type of projects

Source: Berkeley Carbon Trading Project’s Voluntary Registry Offsets Database. Based on purchased carbon offsets’ volumes.

Why are carbon offsets so divisive?

During COP26, carbon offsets were a focus of debate and revived the fear from climate campaigners of interpreting Article 6 of the Paris Agreement as a mandate to develop carbon offsets further, rather than applying pressure on entities to cut back their gross emissions. The final deal agreed by governments aims to implement Article 6 as a rulebook for carbon markets, marking a significant step in the development of the burgeoning market for carbon credits by providing a consistent and transparent framework. The core principle of VCOs is so-called additionality, whereby GHG reductions must come over and above those realised by business-as-usual mitigation activities and policies for climate transition. This would be done through projects that would be uneconomic without the funding derived from carbon offset credits. Other criteria for VCOs include:

- Accountability – measurable and verifiable.

- Irrevocability – permanent impact over time

- Assurance of no harm – no incremental CO2e emissions over the entire value chain and no harm caused in other sustainability domains (biodiversity, social).

The verification of these factors is complex and subject to interpretation, especially on additionality. Organisations verifying the criteria include Gold Standard, Climate Action Reserve, Verified Carbon Standards, and the American Carbon Registry, who all label the credits as Verified Emission Reductions (VERs). But the respective standards vary and, whereas CERs are eligible for both mandatory and voluntary markets, VERs can be used only in the voluntary market.

The quality of the underlying project is a key driver of the VER credit price, but given the smaller scale of the voluntary market, pricing can be unduly influenced by speculative buyers or old and often poor-quality credits. This creates a significant pricing divergence between the voluntary and the mandatory markets, the latter largely controlled by regulators. As a result, voluntary market pricing appears to have decoupled from the real cost of the underlying projects.

Recognising the problem, the Intergovernmental Panel on Climate Change (IPCC) has stated it is essential to have an ambitious carbon price to influence changes in practice. The Institutional Investors Group on Climate Change (IIGCC) has urged caution, while the SBTi (Science Based Targets initiative) does not take voluntary offsets into account in company science-based targets for emission reductions. Lastly, there can be double-counting issues where a government wants to claim recognition for offsets that it then sells onto to another sovereign.

There are benefits from appropriately priced, good quality VCOs and the role these can play in financing climate transition. But the current debate is healthy to avoid the unintended consequences of the existing structure.

How to consider carbon offsets in investment

Decarbonisation within an entity’s own value chain is the absolute priority and starts at the level of gross emissions. As such, not only should the scale and scope of the use of carbon offsets in an entity’s decarbonisation pathway be considered, but also how they impact strategic decisions. For example, is the cost of buying carbon offsets at the expense of funds that would otherwise be spent on decarbonisation, climate mitigation or adaptation?

While the current data capture on the specifics around carbon offsets remains weak, we note that the topic is increasingly highlighted in climate engagement, and company management teams are under pressure to outline the scale, scope and strategy of offsets.

What is the future of carbon offsets?

We expect the debate around carbon offsets to persist after COP26. Collective intelligence is evolving around the climate impact from verified carbon offsets, criticism is shaping standards, and companies are being forced to formally articulate, measure and report their gross and net decarbonisation strategies.

The Task Force on Scaling Voluntary Carbon Markets and the Voluntary Carbon Markets Integrity Initiative are two major initiatives to shape this market. The first will focus on the standardisation of the market, while the second will address the issue of integrity; both will touch on disclosure. COP26 is likely to further accelerate an already fast-evolving segment, especially as we approach the inclusion of Scope 3 emissions in targets.

While we at Allianz Global Investors continue to consider the best avenues to capture the data around offsets, we use engagement as the primary method for understanding the scale and scope of their use by invested companies. This engagement is done either bilaterally with invested companies or through collective initiatives, including the IIGCC.

Direct and gross decarbonisation remains our priority, but a refined and evolving carbon offset market has a role to play in assisting the pathway. Ultimately, for carbon offsets to have an impact by 2050, there needs to be a robust mechanism for making sure decarbonisation targets are more than just accounting adjustments.

Sources:

1 Equivalent because it also includes other greenhouse gases such as carbon dioxide, methane, nitrous oxide.

2 Source: Ecosystem Marketplace, Refinitiv

3 Source: Taskforce on Scaling Voluntary Carbon Markets

4 Source: Ahtna kanas: How-trees-can-pay-off-when-you-leave-them-standing.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Equities have tended to be volatile, and do not offer a fixed rate of return. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bond prices will normally decline as interest rates rise. The impact may be greater with longer-duration bonds. Credit risk reflects the issuer’s ability to make timely payments of interest or principal—the lower the rating, the higher the risk of default. Emerging markets may be more volatile, less liquid, less transparent, and subject to less oversight, and values may fluctuate with currency exchange rates. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication’s sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP (Australian Registered Body Number 160 464 200) is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

1929844