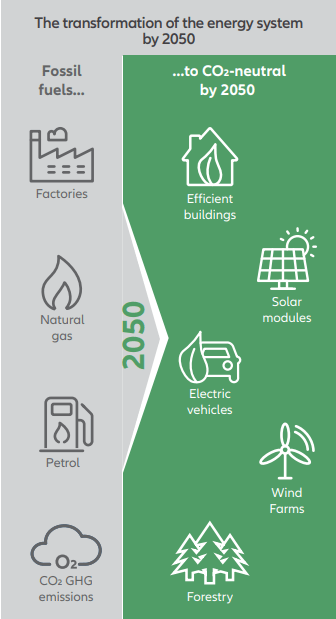

Switching the energy transition to sustainable gears

How investments in solutions for more sustainable energy generation, efficient energy storage and consumption can help accelerate the clean energy transition.

Key takeaways:

- More rapidly advancing climate change, and the drive for energy independence triggered by the invasion of Ukraine by Russian armed forces are the main drivers for the transition

- An acceleration to more sustainable forms of producing, consuming, and storing energy can be observed globally

- The consensus to transform the current energy setup has never been greater

- Investments in companies that provide solutions for cleaner energy generation, efficient energy storage and sustainable energy consumption can help accelerate and shape this transition, whilst at the same time offering attractive investment angles

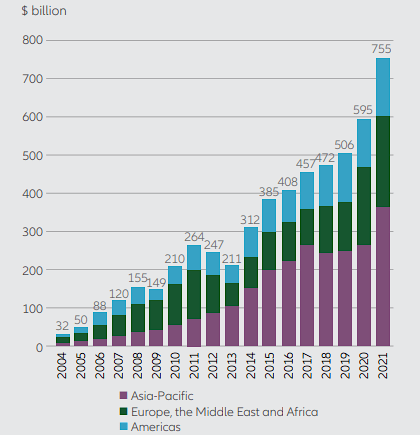

Global investments in green transition are picking up

According to recent analysis,1 in 2021 global investments in the energy transition climbed up to a new record level of USD 755 billion, with renewable energy topping the list with USD 366 billion committed in 2021, an increase of 6.5% compared to 2020.

With investments totalling USD 273 billion in 2021, the electrified transport sector ranked second, driven by a 77% year-on-year-growth rate in spending on electric vehicles and EV-infrastructure.

Looking at the growth path of energy transition investments from an economic area perspective, the Asia-Pacific region stands out twice over: with USD 368 billion it’s not only the zone that recorded the highest investments worldwide, but also the region that with an increase of 38% showed the strongest surge in 2021. EMEA takes second place, with clean energy investment in 2021 adding up to USD 236 billion, an increase of 16% compared to the year before. The Americas, lastly, contributed USD 150 billion in 2021 to the transition to a fossil fuel-free global economy, an increase of 21% compared to 2020.

Broken down by single countries, China invested most in energy transition, with funding worth USD 266 billion in 2021, followed by the US with green energy investments totalling USD 114 billion, and then Germany with USD 47 billion invested in the clean energy transition.

Global investment in energy transition by region

Source: BloombergNEF, as of January 2022.

Larger capital flows, lower costs, and a still substantial funding gap to reach 1.5° C target

According to REN21’s Renewables 2021 Global Status Report, in 2020 global investment in new clean energy capacity reached USD 303.5 billion, an increase of 2% compared to 20192.

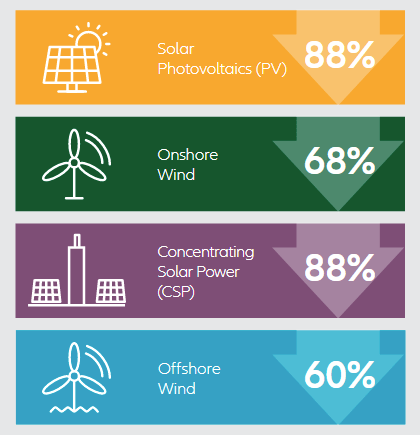

In parallel, expenditures for onshore and offshore wind and for solar power, in 2021 experienced double digit drops of 13% and 15%, respectively, on a year-on-year basis, as projections of the International Energy Agency3 show. In the same year, a remarkable proportion of 2/3 of newly installed renewable power had lower costs than the cheapest fossil fuel-fired option in G20.4

Over a period of more than a decade the decline of green electricity costs is even more significant.

Considering the favourable development of clean energy on the cost side, cautious optimism seems to be appropriate, especially as in parallel, investments in clean energy have been picking up.

But current funding levels are still far from sufficient to develop and scale up already existing and new lowemission technologies that help smooth the transition of the energy system.

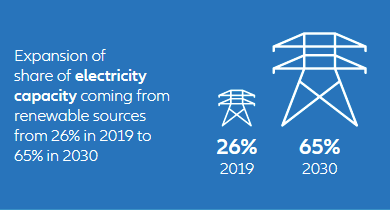

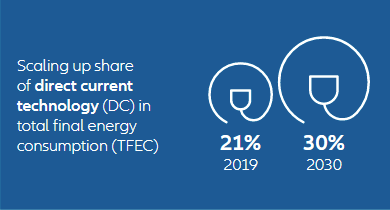

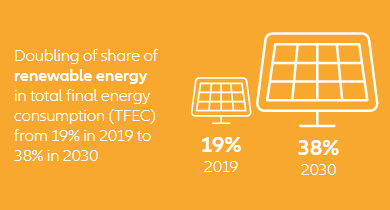

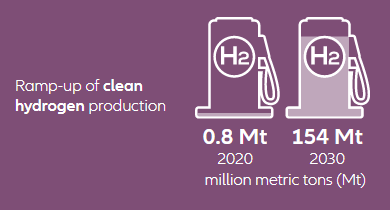

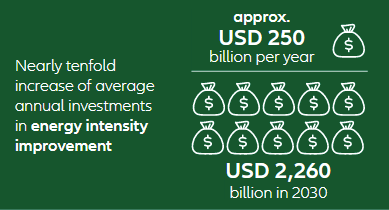

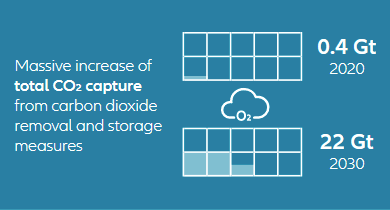

Parameters that could pave the way to achieve 1.5°C target by 2030

Setting sustainable levers in motion

According to the International Renewable Energy Agency’s (IRENA) World Energy Transitions Outlook 2022 Report, the 1.5°C Scenario will require an immense increase on current funding levels within this decade.5

Capital markets and private investors will play a vital role here in raising the major part of the additional capital needed to facilitate and accelerate the clean energy transition, to significantly increase the share of renewables in the overall energy mix.

Matching the gap between generation of energy use and keeping the grid stable calls for innovative solutions. These new-frontier technologies will reach marketability, and help to ensure a smooth transition. In addition, energy storage solutions like battery technology and hydrogen technology will become more important in future. As well as just storing energy, hydrogen might help to decarbonise carbon-heavy industries (steel & cement) and can be used as a substitute for natural gas. Therefore, the creation of a hydrogen-based economy remains an important pillar.

Routes to renewables

During recent years governments and entities world-wide have started pushing the green accelerator pedal by freeing up considerable amounts of capital to help bring their countries and the world back on the 1.5°C maximum-warming track.

USA

With the Inflation Reduction Act passing both the US Senate and the Congress in August, the United States adopted an extensive legislative package that according to US President Joe Biden “makes the largest investment ever in combatting the existential crisis of climate change”.6

With almost USD 370 billion of climate spending over the next ten years and the objective to significantly reduce energy costs, increase cleaner production, and cut carbon emissions by approximately 40% by 2030, this bill represents quite an historic feat, and “does about two-thirds of the remaining work needed to close the gap between current policy and the nation’s 2030 climate goal”7 i.e., to halve emissions by the beginning of the next decade.

China

In its 14th Five-year plan for renewable energy development8 the People’s Republic has set ambitious goals to foster the green and low-carbon transformation of the country by 2025 and beyond. Besides the ambition to achieve carbon neutrality by 2060, and the gradual reduction of carbon dioxide emissions, China is also striving to boost the proportion of renewables in its overall power consumption and installations.

China’s 2025 renewable energy development roadmap

|

Category |

Unit |

2020 |

2025 |

|

Share of renewables in total power |

% | 28.8 | 33 |

|

Share of non-hydro renewables in total power consumption |

% | 11.4 | 18 |

|

Renewable power generation |

TWh | 2,210 | 3,300 |

|

Use of renewable energy for purposes other |

kt stce* | — | 60,000 |

|

Total renewable energy consumption |

Mt stce* | 6,800 | 10,000 |

|

Total installed wind and solar generation |

GW | 534.9 | Over 1,200 |

*stce = standard coal equivalent.

Japan

With its Green Growth Strategy,9 the country has taken up pressing climate change challenges. Backed by the Green Innovation Fund worth 2 trillion yen (approx. USD 15.1085 billion), the program aims to, amongst other things:

- install 10 GW of offshore-wind power by 2030, and 30-45 GW by 2040.

- establish carbon-free hydrogen production technology for high-temperature gas-cooled reactors (HTGR) in 2030.

- have electrified vehicles making up a 100% share of new passenger car sales in 2035.

- achieve carbon-neutral semiconductor/information and communication industries by 2040.

UK

The UK Government’s Department for Business, Energy and Industrial Strategy “Ten Point Plan for a Green Industrial Revolution”10 includes, among other measures:

- a GBP 12 billion fund of public money to support the lowcarbon energy industry, and a commitment to securing 40GW of offshore wind power capacity by 2030 (up from around 10GW in 2021).

- a GBP 1 billion fund to “support the electrification of UK vehicles and their supply chains” plus GBP 1.3 billion to speed up the rollout of EV charging infrastructure.

- a GBP 240 million Net Zero Hydrogen Fund to build up 5GW of low-carbon hydrogen production capacity by 2030.

Germany

The German Federal Government recently committed an additional EUR 8 billion11 to promote the expansion of renewable energies and related abatement measures, including the funding of:

- EUR 860 million for “green steel” and transitioning steel production to green hydrogen.

- EUR 95 million for promoting offshore electrolyser systems, and doubling electrolysis capacity to 10 GW by 2030.

- EUR 5.5 billion for the energy refurbishment of residential buildings, and climate-friendly new construction.

- more than EUR 1 billion for improving medium to longrange charging infrastructure for e-vehicles.

Spain

A big Spanish utility has recently announced investments close to USD 5 billion for, amongst other things, the adaption of natural gas infrastructure for the handling of hydrogen and for the production of renewable hydrogen. But also, on a non-corporate level, Spain is following an ambitious agenda to become Europe’s hydrogen frontrunner.

The country’s Renewable Hydrogen Roadmap,12 for instance, envisages installing 4 GW of electrolyser capacity by 2040 (equivalent to the capacity of four large coal-fired power plants), in parallel with getting 150-200 fuel cell buses and 5,000-7,500 light and heavy-duty fuel cell transport vehicles onto Spanish roads, accompanied by 100-150 public access hydrogen stations.

European Union

The European Commission’s REPowerEU Plan13 is an additional response to the market disruption caused by the conflict between Russia and Ukraine. The double urgency to transform Europe’s energy system is based on following the Paris 2015 climate agreement, and ending the EU’s dependence on fossil fuels from Russia, adding up to around 100 billion Euro per year. To “fast forward the green transition” and to quickly lessen the EU’s dependency on Russian fossil fuels, the REPowerEU Plan contains, amongst other measures:

- the doubling of solar photovoltaic capacity by 2025, and installation of 600GW by 2030.

- setting a target of 10 million tonnes of domestic renewable hydrogen production and 10 million tonnes of imports by 2030, as a replacement for natural gas, coal and oil in hard-to-decarbonise industries and transport sectors.

To emancipate Europe from its dependence on Russian fossil fuels, the EU Commission expects a funding gap of Euro 210 billion within the next five years, emphasising that “these investments must be met by the private and public sector, and at the national, cross-border and EU level.” On the plus side, delivering the REPowerEU objectives could lead to savings of nearly Euro 100 billion per year, not least because of the drastic cutback of Russian fossil fuel imports.

NextGenerationEU

NextGenerationEU: Key Features

Source: AllianzGI. All amounts are in billion EUR, in current prices, as of November 2020.

Identifying clean energy transition frontrunners and beneficiaries

Despite the encouraging growth of investments in sustainable energy solutions, current funding levels are still insufficient to tackle the multifaceted challenges related to the clean energy transition. From an investor’s angle, the projected and urgently needed rise of clean energy spending in the next years opens up interesting possibilities to participate in the growth prospects of enablers and beneficiaries of the energy transition process. Investments in solutions that deliver on changing energy consumption patterns, and the resulting new demand dynamics are just two of several pathways to support energy transition along the entire value chain.

We look at companies around the globe with long-term potential that provide solutions to cleaner energy generation, efficient energy storage and sustainable energy consumption along the value chain, and at the same time contribute to the ecological and social goals of the UN SDGs.

We also identify opportunities arising from the development of innovative technologies like hydrogenbased energy supply, or other forms of energy storage or CO2-reducing tech innovations that are still in their infancy and are yet to unfold their benefits – not least considering currently rising energy prices as a temporary side effect throughout the transformation phase.

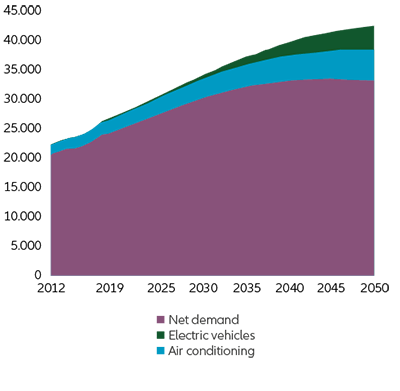

Demand for electricity will double by 2050

TWh

Shift in energy consumption will accelerate the process of electrification by 2050*

Source: New Energy Outlook 2019, BNEF 2019 June; Global Energy Perspective, McKinsey 2018 November.

*Percentage increase refers to the acceleration case vs. reference case.

1 BloombergNEF: Energy Transition Investment Trends 2022

2 IRENA: Competitiveness of Renewables Continued amid Fossil Fuel Crisis

3 IRENA: Investment flows, chapter 05

4 IRENA: Competitiveness of Renewables Continued amid Fossil Fuel Crisis

5 IRENA World Energy Transitions Outlook 2022, page 56

6 The White House briefing room

7 REPEAT Preliminary Report 2022

8 China Energy Portal

9 METI Ministry of Economy, Trade and Industry

10 The Ten Point Plan for a Green Industrial Revolution

11 Federal Ministry of Finance

12 MITECO Ministerio para la transición ecológica y el reto demográfico

13 European Commission: REPowerEU

14 European Union: NextGen EU

ADM 2396509