Navigating Rates

Fixed Income Quarterly:

Fixed income in flux as opportunities emerge

Shifting paths of inflation, interest rates and economic growth are creating a complex market environment. As central banks balance taming inflation with containing financial risks volatility in markets is likely to persist – but we see select openings arising across government and corporate bonds.

Key takeaways

- We believe the versatility and higher yields of fixed income make it a potentially attractive option in this transitional period for markets.

- With the Fed’s hiking cycle maturing and recession still a risk, we think US Treasuries look good value in the belly of the curve.

- We think investors can find opportunities in emerging markets and Asian bond markets, where the growth and inflation outlook is more positive than in developed markets.

- At a company level we see continued resilience from investment grade issuers, though after recent spread rallies we think single name selection should be prioritised in high yield.

The second quarter of 2023 once again demonstrated the uncertainty investors face on the path of monetary policy and the broader macroeconomic outlook. But this period also hinted at the opportunities fixed income may offer in the second half of the year.

As recently as mid-May, markets were pricing in a high probability of a September interest rate cut from the US Federal Reserve. Instead, we have seen a strengthening of the higher-for-longer rates narrative with the Fed indicating at its June meeting that more rate hikes could yet be required. This is a global theme, with markets also adjusting to more hawkish stances in Canada, Australia and the UK.

In our view, the downturns or recessions that many expect to hit advanced economies continue to be delayed by factors such as excess liquidity from Covid-era stimulus supporting consumer spending. A fall in commodity prices also helps growth. However, many leading economic indicators continue to deteriorate and inflation expectations (based on 5-year forwards) are low and steady around 2.5% in both the US and Europe.

We have higher conviction today than we had three months ago that we will see a steepening US yield curve, and we are also more convinced of the potential benefits of adding duration risk in the US. A rally in investment grade (IG) corporate bond spreads means we think they are now generally trading closer to fair value, but the carry is attractive and we see some value left in the European market.

Economic and policy divergence from country to country continues to offer bond investors a broad opportunity set. The versatility and higher yields of this asset class make it a potentially attractive option in this transitional period for markets.

Strategy conclusions:

Core rates |

|

|

Country |

Favour higher real yields in cross-country spread trades; wait-and-see on euro zone periphery until more visibility on downside tail risks to the economy |

|

Duration |

Gradually add to “belly” of US yield curve (around 5yr+ duration); more patience in euro zone as higher risk of repricing |

|

Yield curve |

Higher conviction in US curve steepening (5yr-30yr) given more advanced US credit tightening cycle than euro zone |

|

Inflation |

Neutral stance on euro zone as base effects continue to dominate; US real yields look attractive at current levels |

|

Currency |

Less macroeconomic scope for broad-based USD rally; long JPY as growing pressure for BoJ policy normalisation |

Corporate credit |

|

|

Investment grade (IG) |

Maintain small overweight for carry, valuation shift from cheap to fair, less scope for spread tightening from here |

|

High yield (HY) |

Underweight beta, good all-in-yields but tight spreads, favour short duration BBs, relative value in Asia ex-China |

|

Hybrids |

Stay cautious on REITs, sector under pressure, positive on logistics, neutral on residential/hotels, negative on retail |

|

Securitised |

Short-dated covered bonds may feature less spread volatility vs. sovereigns, supranationals, agencies, corporates |

|

Region |

Historically better USD excess returns in downturns but extra spread in same-rated EUR issues; Asia IG looks solid |

|

Sector |

Reducing cyclical bias in HY; in IG overweight US/EU financials, US utilities, underweight industrials, food, chemicals |

Emerging market debt |

|

|

Hard currency sovereign |

Distress looks well contained within smaller/frontier markets, scope to build exposure to select turnaround stories |

|

Local currency sovereign |

Prefer countries with high policy rates, softening inflation, solid balance of payments, eg, Brazil, Mexico, Thailand |

|

Hard currency corporate |

Looking to add opportunistically in Asia primarily in higher quality, defensive names; LatAm very rates-sensitive |

These views are updated regularly to reflect changing market conditions and are independent of portfolio construction considerations. Past performance is not a reliable indicator of future results.

Global growth momentum set to remain weak

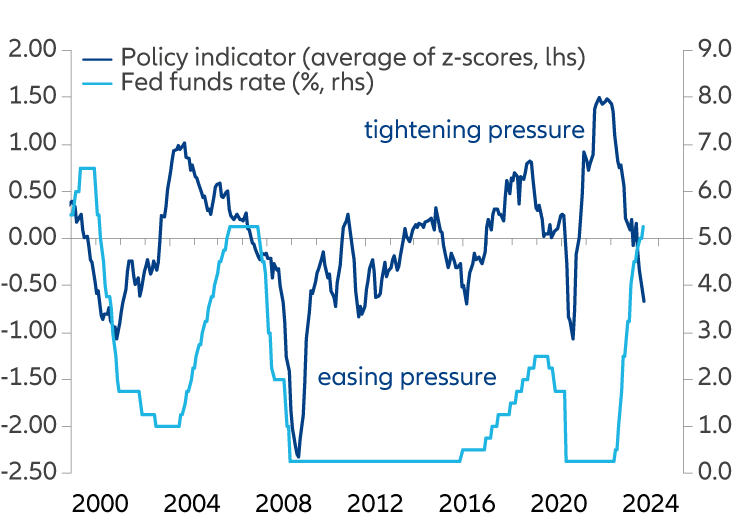

While the US Federal Reserve’s interest rate hiking cycle is maturing (see Exhibit 1), we think the generally restrictive global monetary policy stance will continue to challenge the global growth outlook over the next 6-12 months. Relative to recent economic cycles, central banks remain reluctant to pivot away from this restrictive stance as core inflation remains well above central bank targets and labour markets are still tight.

As a result, we see global growth continuing to running below its trend rate over the coming three to six months, despite recent signs of a stabilisation in activity after the banking stresses in March. However, bank lending surveys suggest credit supply and demand metrics are deteriorating. We expect the monetary and credit tightening that began early last year to start showing up in hard economic data as we head through the second half of 2023.

Over a one-year horizon, a US recession caused by high policy rates, tightening lending standards, falling disposable income and weakening corporate profitability represents our base case scenario. However, we recognise that at the current juncture a relatively shallow recession seems the most probable scenario.

The Chinese economy seems to have lost any reopening momentum as both growth and inflation indicators remain anaemic,1 forcing the People’s Bank of China (PBoC) to initiate further policy easing. Chinese growth prospects continue to be challenged given private sector balance sheets remain overleveraged.

Market implications

- Consider US Treasuries: as we move into the second half of 2023, clouds are gathering over the US economy and the Fed’s hiking cycle is maturing. Substantial rate increases have been delivered, real rates are in positive territory across the curve, and expectations for terminal rates are high compared to the perceived neutral rate. We are cognisant that volatility in global fixed income markets will remain elevated in the coming quarters, so we see value in the belly of the US Treasury curve.

- Focus on real yields: with persistent uncertainty around the outlook for inflation, we think investors could focus on the positive “real yields” (returns from interest payments after taking account of inflation) available in jurisdictions where rate hike cycles are more mature. Since last quarter, the UK has now joined the US, New Zealand and Mexico on the list of sovereigns which we think offer attractive real yields.

- Seek out EM bonds: EM assets have historically provided strong returns for investors at the end of Fed hiking cycles, though we are mindful of differences between this economic cycle and previous iterations. Inflation in EM economies has been rolling over and the growth outlook is also brighter than in developed markets. At an asset class level, index yields make a compelling total return proposition, with a high carry providing a buffer for potential yield increases. Overall, the carry of the asset class is still appealing for hard currency sovereigns and corporates, which should continue to attract investor inflows given institutional underinvestment in emerging economies.

- Be wary of euro sovereigns: further ECB tightening increases recession risks and the likelihood of a risk-off scenario. Following strong performance from European periphery markets in the first half of the year, we are now looking to build a more defensive positioning on European sovereign debt.

Exhibit 1: The US Federal Reserve hiking cycle is maturing

Source: Refinitiv Eikon Datastream, Bloomberg, Allianz Global Investors GmbH. Data as at June 2023.

Inflation easing but “higher for longer” looms large

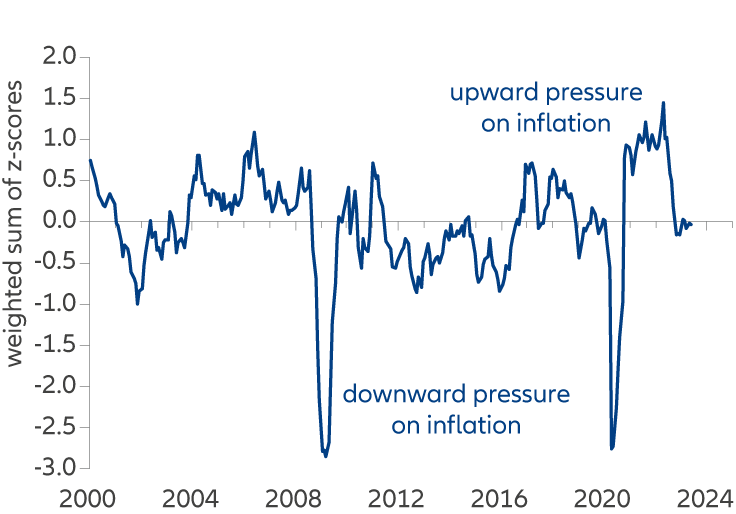

Headline inflation rates have been moderating across the globe since the start of the year (see Exhibit 2), though core inflation remains stubbornly high across many G10 economies as labour markets are historically tight. However, US survey data and our proprietary wage pressure indicator point towards a deceleration in the pace of wage growth. We expect this to pave the way for a decline in core inflation rates into year-end. Core inflation pressures are likely to remain stickier in the euro zone than the US given relatively looser financial conditions and an easier fiscal stance in the former. Therefore, we expect more risks of upward repricing in front-end rates in the euro zone compared to the US.

In the US, while we believe the terminal rate is around 5.5%, there is a risk that forward curves may still be under-pricing the willingness of the US Federal Reserve to maintain a higher-for-longer policy stance. In this context, the key risk for the second half of 2023 may stem from the misalignment between the Fed’s projections for the path of interest rates and inflation compared to prevailing market pricing. Should inflation remain stickier than the market currently expects, rate cuts for 2024 risk being priced out.

In the euro zone, concerns that core inflation could remain well above the European Central Bank’s target by the end of 2023 continue to drive a near-term hawkishness in the central bank’s policy stance.2 Despite the recent aggressive ECB rate hikes (and the market’s pricing of a terminal rate above 3.75%), we think real interest rates (rates adjusted for inflation) in the region remain too low to bring inflation towards the 2% target by the end of 2023.

In emerging markets (EM), a moderation in inflationary pressures suggests many emerging market central banks are close to the end of their tightening cycles. Among those central banks, Brazil and Mexico emerged from the 2021/22 inflation shock with strengthened credibility as they started hiking aggressively ahead of G10 central banks. We expect these central banks to start the easing cycle ahead of the developed world as real rates are in restrictive territory and inflation is rolling over.

Market implications

- Settle for carry in IG: we see IG credit spreads as being rangebound – where they trade between consistent highs and lows – due to the uncertainty of the wider economy and its implications on the corporate and banking sectors. However, investors can still benefit from holding bonds with relatively high yields, or “carry”. Within IG corporates we see most value in euro zone credits, which at 171bps at the index level generally look cheap, while US credit (138bps) and global credit (151bps) look closer to fair value.

- Seek resilience in euro corporates: despite the sharp rise in the cost of production factors, European companies have generally succeeded in improving margins and maintaining profitability, and we do not expect asset quality to deteriorate significantly in the coming months. Fundamentals for the sector are healthy, earnings are solid and capitalisation is adequate. Areas with potential downside risks include construction, real estate and household consumption.

- Exercise caution in high yield: The recent earnings season was mixed with greater performance dispersion within rating bands and sectors. Lending standards are tightening, funding costs are rising and credit metrics are deteriorating but HY spreads have continued to rally, particularly in lower-rated credits. We see signs of potential spread widening to come with recession on the horizon in both the US and Europe. Single name selection should therefore be prioritised over sector allocation – look for companies with lower leverage and higher equity cushions which are less susceptible to higher costs of funding.

- Examine Asian fixed income: Asia investment grade has outperformed US IG and we expect some consolidation at current levels. Asia IG technicals remain strong and the supply outlook is sanguine, which should support spreads. The carry and yield in BBB rated bonds in particular look attractive. A cautious approach to high yield bonds also applies to the Asia market, though we think valuations in ex-China HY remain attractive versus US HY.

Exhibit 2: Inflation pressures have been diminishing

Source: Bloomberg, Allianz Global Investors GmbH. Data as at June 2023.