Summary

Propelled by governments’ bid to support the economic recovery from Covid-19, booming demand for digital services and the push to a greener economy, infrastructure spending is ramping up. That should create opportunities for institutional investors seeking stable, long-term cash flows.

Key takeaways

|

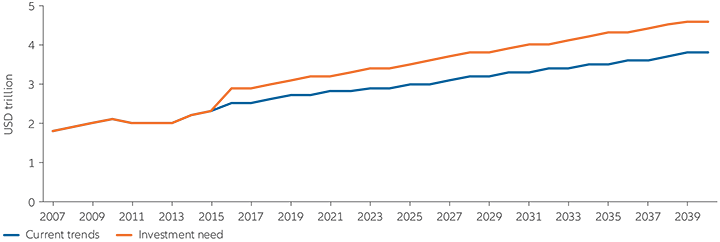

From financing bridges to broadband, infrastructure debt is a growing asset class with much to offer investors. As well as its built-in illiquidity premium – an additional compensation for investors in return for tying up investment in an asset that cannot easily be converted to cash – infrastructure debt also offers portfolio diversification opportunities and a tangible way to boost economies and improve societies. And the long-term prospects are strong. Global infrastructure investment needs to rise to USD 94 trillion by 2040 to keep pace with economic growth and meet the UN Sustainable Development Goals, estimates the G20 Global Infrastructure Hub (see Exhibit 1). To seize the opportunities in the infrastructure-debt realm, we suggest that investors focus on five areas – from rising interest rates to regulation.

When financing a company or project, investors need to consider what the terms might be in the future when repayment is due. Issuers have taken advantage of the low interest rate environment of recent years to increase leverage.

Higher interest rates could pose a hurdle for many companies - including those in the infrastructure sector - that need to refinance their debt in an environment of much higher interest rates. Will they then be able to service their debt while maintaining their investment grade status?

At the same time, even though rates are on the rise, we’re still in a low-yield environment. Under these conditions, infrastructure debt can still provide significant benefits to investors with a buy-and-hold mentality. Infrastructure projects are inherently long-term illiquid sustainable assets, and their illiquidity premium may provide superior yields to many sovereign or covered bonds.

How we can help

As Europe’s first infrastructure debt financier, Allianz Global Investors has the experience to carry out the necessary due diligence to manage risks and understand how these conditions may impact our investments. With our focus on longer-dated duration assets, we seek to actively navigate the potential for rising interest rates by putting in place structural protections that can provide capital stability to investors.

Passenger traffic came to a virtual standstill when the pandemic broke out, hitting transport infrastructure. Many airports, toll roads and other "essential assets" did not have sufficient ongoing cash flow to continue servicing their debt.

In some cases, shareholders have been asked to step in, while other companies have had to negotiate with their banks to extend the liquidity line or draw on existing credit lines to bridge this period. Therefore, the liquidity position of these assets is a key factor. Consider these different sectors:

- Airports: passenger numbers are likely to recover to pre-pandemic levels, but airports with a high share of intercontinental traffic will need more time. We expect the impact on airports to continue for three years before possibly returning to 2019 levels

- Road traffic: traffic volumes fell by 90% during the lockdowns. After the restrictions were lifted, however, traffic quickly returned to pre-pandemic levels.

- Public transport: this sector has suffered, but has shown great resilience, thanks to the support and financial backing of municipalities. These important services will continue in some shape or form as people return to normal life after the pandemic.

How we can help

The expertise and deal sourcing capabilities of our Infrastructure Debt team allowed us to successfully navigate the market turbulence caused by Covid-19. We added EUR 2.2 billion of investments in 2020. We were able to build on that in 2021 by completing 14 transactions, amounting to EUR 2 billion. In 2022 we are identifying opportunities for our clients from an expected increase in the volume of mergers and acquisitions as businesses recover.

Exhibit 1: Global infrastructure spending: current trends vs investment need

Source: Global Infrastructure Outlook outlook.gihub.org

Many investors are interested in green bonds and renewable energy investments as part of the push to a carbon-neutral economy. This also reflects the increasingly widespread pressure to take ESG (environmental, social and governance) considerations into account in investment decisions. The current political situation also underpins the drive to significantly increase the share of renewable energy.

Green bonds, which support specific climate-related projects and renewable energy, are being swamped by demand. As a result, financing terms have softened so that some can no longer be considered investment grade. This may mean that in some transactions where there is strong investor demand, lenders receive less protection. Therefore, investors should be very selective in choosing their transactions.

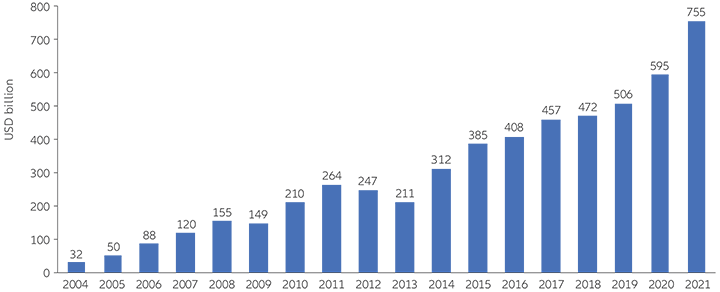

Over the years, the industry has made significant progress in its understanding of ESG. However, investing in ESG "friendly" assets only leads to net zero up to a point. Sustainability-minded investors should favour investments that support a holistic transformation of the company and should seek to support other issuers on their "green" journey. We see particular opportunities in the area of emerging energy technologies – such as batteries, hydrogen and biofuels – as companies can invest in new areas and thus reduce their CO2 emissions (see Exhibit 2). Such investments are usually debt financed to optimise the return on equity.

How we can help

We help the companies we invest in focus on a holistic transformation, while recognising that overnight change can be difficult. For example, when investing in an energy company we may seek to provide covenants within financing documents pledging to increase the company’s use of renewable energy – hence, moving the business to a more sustainable footing. We are actively seeking similar opportunities where we are helping to put our economy on a net-zero trajectory.

Exhibit 2: Global investment in the energy transition

Includes investment in sustainable materials, carbon capture and storage, hydrogen, nuclear, electrified heat, electrified transport, energy storage and renewable energy

Source: BloombergNEF about.bnef.com/energy-transition-investment

The infrastructure debt asset class is being affected by the increasingly large focus on regulation overall, and by regulators’ desire to provide investors with more transparency and information. For example, the European Commission is intensively pushing the issues of sustainability and climate change – and, like other asset classes, infrastructure debt is having to adapt.

- One result is the EU taxonomy - a classification system designed to provide a common wording and a clear definition of "sustainable" business activities. This is intended to guide investments to achieve the European Union's 2030 climate and energy targets.

- Meanwhile, the Sustainable Finance Disclosure Regulation (SFDR) requires funds to disclose how they are increasingly incorporating sustainable practices into their activities and clearly defines which strategies qualify as sustainable investments.

Infrastructure debt investors can play a critical role in addressing the climate crisis and achieving carbon neutrality. However, the challenge with unlisted companies is often that ESG information is not as easily accessible as it is for listed firms. In addition, many industries have not yet defined common methodologies, reporting guidelines and metrics, making it difficult to assess progress. Investors, therefore, have to spend a lot of time and resources gathering information from borrowers on areas such as greenhouse gas emissions or alignment with the EU taxonomy.

How we can help

We work hard to ensure we fully understand the EU taxonomy and other regulations which are changing at increasing speed. As there’s no standard way of accessing information, we conduct our own detailed due diligence and we are also an active member of the GRESB, (Global ESG Benchmark for Real Assets) an investor-led organisation which provides a solid database of ESG information collected from issuers. This can help investors focus on building a portfolio of sustainable assets.

In the infrastructure sector, digital assets are in greater demand than ever before. Fibre-optic networks and data centres are particularly sought after. However, the Covid-19 pandemic, with a sharp increase in video conferencing for businesses and streaming services for the home, also highlighted the deficits in digital infrastructure. In Germany and the UK, for example, fibre-optic represents only around 6% of total fixed broadband, according to the OECD. That’s compared to more than 80% in the market leaders of South Korea and Japan. But Germany, the UK and many other large economies are seeking to significantly ramp-up their broadband capabilities.

However, there are many more nuances to consider when it comes to business models. This is because competition for digital infrastructure has increased significantly. For investors, the market segment presents exciting opportunities, but also harbours risks. Long-term investors therefore need to take a close look at the assets they invest in to ensure that they are appropriately positioned to respond quickly and adequately to a changing environment as market conditions change.

How we can help

We are focused on helping our clients navigate a fast-growing sector with dynamics that may be unfamiliar to some investors. With a traditional infrastructure provider, such as a utility supplier there is often certainty about revenues as homes are already connected to the power grid. But with a digital asset, like a fibre-optic network, there is sometimes less revenue stream clarity as the network is still being built. We aim to manage such risks by imposing key performance indicators – like minimum number of houses connected – that must be met before we consider financing.

Outlook

The current market environment offers opportunities to build exposure to infrastructure debt, an asset class with a vital contribution to global societies and economies.

As the world recovers from Covid-19 and governments and companies pursue sustainable growth paths, we expect a pick-up in merger and acquisition activity, typically financed by debt. At the same time banks, traditionally one of the largest infrastructure debt financiers, are continuing to retrench from long-term funding markets because of regulatory hurdles. That opens the door for other institutional investors.

While there will be challenges, such as rising interest rates, the sector can serve as a long-term sustainable asset through which investors can help fund the infrastructure to keep economies moving.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested.

Investments in Infrastructure debt are subject to adverse economic & regulatory risks affecting infrastructure companies. Infrastructure issuers may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers, operational or other mishaps, tariffs, and changes in tax laws, regulatory policies, and accounting standards.

Incorporating alternative investments into a portfolio entails substantial risks and is not suitable for all investors. Investors must be aware that an investment in infrastructure is highly speculative, and it is possible to lose your entire investment. Investments in Infrastructure are subject to adverse economic & regulatory risks affecting infrastructure companies. Infrastructure issuers may be subject to regulation by various governmental authorities and may also be affected by governmental regulation of rates charged to customers, operational or other mishaps, tariffs, and changes in tax laws, regulatory policies, and accounting standards. The market for infrastructure investments is highly illiquid, which could prevent an investor from purchasing or selling these investments at an advantageous time resulting in a loss to the investor. Investing in a limited number of issuers or sectors may increase risk and volatility.

Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is for Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations and is for information purpose only. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; in HK, by Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; in Singapore, by Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; in Japan, by Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424], Member of Japan Investment Advisers Association, the Investment Trust Association, Japan and Type II Financial Instruments Firms Association; in Taiwan, by Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan; and in Indonesia, by PT. Allianz Global Investors Asset Management Indonesia licensed by Indonesia Financial Services Authority (OJK).

2189494

Want to view more?

Summary

During periods of disruptively high inflation, investors may want to rethink their allocations to certain equity sectors and investment styles. For example, the energy and consumer discretionary sectors have historically fared better than consumer staples and utilities during inflationary periods. The value, momentum and quality styles have also done well, on average.

Key takeaways

|