Active is: Contributing to climate goals

Are all net-zero goals created equal?

Summary

The race is on for companies to declare their commitment to achieving net-zero emissions, as outlined in the Paris Agreement. But given the various inconsistencies in how the phrase is understood, what does “net zero” really mean – and how should progress towards this goal be measured?

Key takeaways

|

Once a piece of jargon used by climate experts, the term “net zero” has swiftly entered the mainstream in the run-up to the UN Climate Change Conference (COP26) in November 2021. Many countries, regions, companies and investors are announcing climate action goals and targeting net zero by a specific date, usually around the middle of this century – per the goals set out in the Paris Agreement on climate change.

Participation in the Race to Zero – an initiative of the UN Framework Convention on Climate Change to rally the largest-ever alliance committed to net-zero carbon emissions – has grown to 4,800 entities since the campaign’s launch in June 2020. Corporate entities account for around 3,000 of this number. This makes it easier for investors to identify those companies that are working towards this goal.

Considering the most recent Intergovernmental Panel on Climate Change (IPCC) report, described as a “code red for humanity”, this acceleration in global mobilisation towards the Paris Agreement objective is an encouraging development. But as investors look to allocate money towards companies contributing to climate transition, it is useful to examine the meaning of the phrase “net zero” and ask whether all net-zero goals are equal.

What is net zero?

The term “net zero” derives from a 2013 IPCC report, which discussed the need to eliminate net greenhouse gas (GHG) emissions to stop global warming. The “net” relates to the balance between emissions generated by human activities and those removed either naturally or artificially through carbon-capture technologies. The report paved the way for the Paris Agreement in 2015, with each signatory pledging to meet the targeted equilibrium – “net zero” – by 2050 at the latest.

The idea of equilibrium sounds like a simple equation. But for investors who want to support this target through the companies they invest in, the parameters around the underlying calculation are more complex, revealing competing definitions around what is meant by net zero.

For instance, a net-zero target is strictly achieved only when the full range of an entity’s activities are included. Yet some companies in some industries (for example, utilities) currently calculate their net-zero activities without including certain geographic regions; in other sectors (such as mining) some companies discount specific assets; while in other sectors (such as telecoms and media) some firms do not include all business structures. However, a best-practice approach should include all business activities across every division of a company, even if timelines may differ between them.

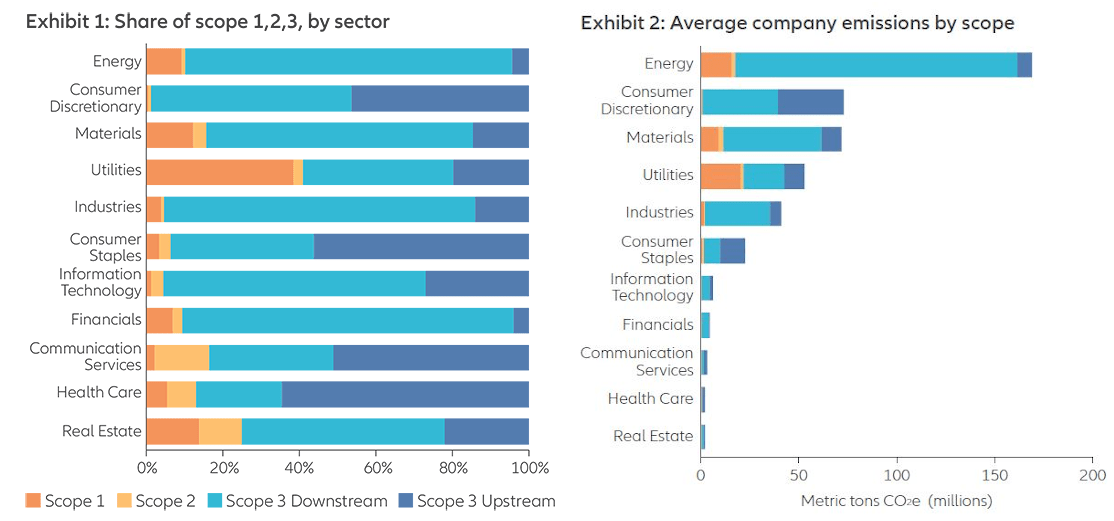

Ensuring that Scope 3 emissions are calculated

In the world of net-zero reporting, there are three classifications of emissions:

- Scope 1: direct emissions from sources that a company owns or controls, for example, emissions from a car manufacturer’s own factory.

- Scope 2: indirect emissions from the generation of energy purchased by the reporting company, for example, emissions relating to the energy used by that car manufacturer.

- Scope 3: indirect emissions produced outside the company’s direct control through its entire value chain – these include emissions from before goods enter the company’s gates (“upstream”), for example emissions resulting from the production of steel needed to build the cars, and emissions resulting from handling, distribution and usage of the final product (“downstream”), for example those resulting from the car’s own fuel consumption.

Scope 3 accounts for a substantial share of total emissions in many sectors, but for many firms it is only partially included in calculations for their net zero targets, if at all. We think this is potentially confusing and frustrating for investors who want to know what types of emissions are being included in net-zero targets, and whether there is clear disclosure around those targets.

At Allianz Global Investors, we actively encourage companies to develop and implement policies and practices to target a fully scoped net-zero commitment. Our recent analysis of a mining company indicated that, while it had committed to net-zero targets for Scope 1 and Scope 2 emissions, it was also able to quantify and disclose a full inventory of Scope 3 emissions, broken down into 15 categories over its entire value chain. The company has now put in place initiatives to reduce full-scope emissions for those Scope 3 categories over which it has some control, such as shipping.

Some sectors currently feel limited pressure to focus on their net-zero activities because they have low Scope 1 and 2 footprints. We expect the focus on monitoring Scope 3 to increase, to ensure equivalence across sectors, and greater alignment with the wider climate effort.

Greenhouse gas (GHG) emissions by sector

Source:

Exhibit 1: GICS sector (based on MSCI World – MSCI 08/06/2021)

Exhibit 2: A carbon dioxide equivalent or CO2 equivalent, abbreviated as CO2e is a metric measure used to compare the emissions from various greenhouse gases on the basis of their global-warming potential (GWP) (source Glossary:Carbon dioxide equivalent - Statistics Explained (europa.eu))

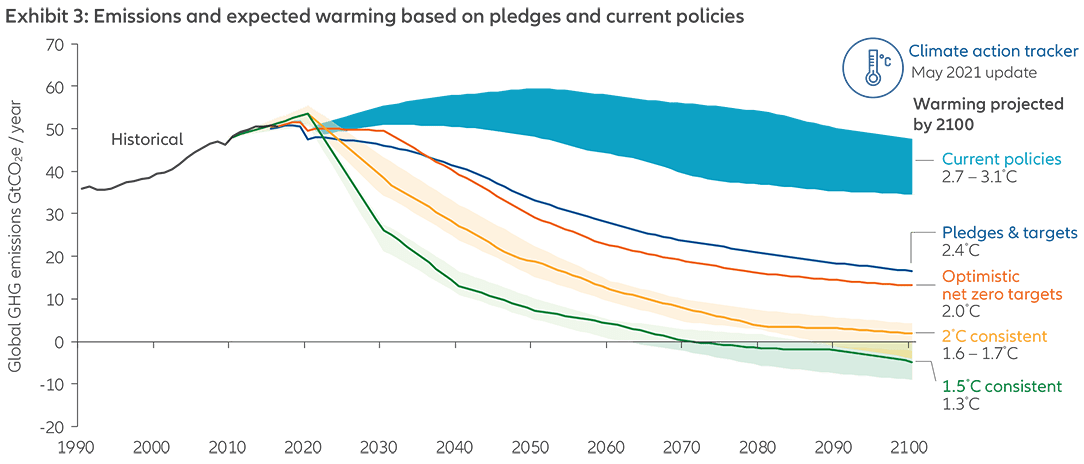

Targeting gross emissions to achieve net zero: timing is key

In many ways, the journey to net zero is as important as the destination. While the target references a net figure in the future, gross emissions must be reduced along the way. The Paris Agreement makes this clear: global CO2 emissions need to be reduced by 50% (from 2020 levels) by 2030 to limit global warming to a 1.5°C increase by 2050. This is a global objective, but the Race to Zero’s requirement is that individual companies “should contribute their fair share to the 50% global reduction”.

Another key component of the Paris Agreement is a pledge to keep temperature increases below a 2.0°C increase over pre-industrial levels – and, if possible, at 1.5°C1. Although this seems like a small difference in temperature, the real-world effects could be massive. As such, the shape of the curve showing cumulative carbon emissions over the period leading up to achieving net zero will likely define the final warming level.

Understanding this curve is fundamental to understanding scenario analysis for investee companies. The definition and communication of an appropriate interim target aligned to the final target is a minimum requirement for any company joining the UN’s “Race to Zero”2. However, a December 2020 study by Oxford University’s Energy & Climate Intelligence Unit (ECIU) showed that only 50% of large companies with a stated net-zero commitment have made such a plan public.

The Science Based Targets Initiative (SBTI) is one of several organisations that help companies ensure consistency in reporting while standing up to increasingly robust scrutiny from investors. Using a scientific framework, the SBTI breaks down and assesses the targeted global trajectory to create sector-specific pathways to reduce emissions. Its recent decision to raise the bar for target validation – from “well below 2°C” to “1.5°C” – underscores the intensified sense of urgency ahead of COP26.

2100 Warming projections

Source: Climate Action Tracker

Carbon offsets: what role do they play on the journey to net zero?

“Carbon offsets” is a catch-all description for all the tools that companies or institutions can use to reduce GHG contributions in one area to compensate for emissions made elsewhere. They are a divisive factor in the net-zero equation. While there is strong consensus about the critical role offsets can play in corporate net-zero strategies, there is still debate around how much they actually contribute. We identify two conditions that should be attached to their use:

- Carbon offsets should not compromise gross emission reduction actions.

- Activities underpinning the claimed offsets should effectively, sustainably and verifiably reduce carbon emissions without undermining other sustainability aspects (such as biodiversity and social priorities).

Carbon offsets add an additional layer of complexity as we engage with companies to assess their progress towards net zero. We need to consider each company’s offsetting activities in their entirety, in the context of the relevant offsetting strategies that are available. Businesses can choose to compensate gross emissions through indirect investment into carbon credits, or through direct investment into lowering emissions or reducing activities – both within and outside their value chain. Options for the latter include carbon capture, utilisation and storage (CCUS).

On a broader level, our view of companies’ climate reporting suggests the use of carbon offsets is not yet meaningful at an aggregated level. However, they are being used increasingly in some sectors, such as financials. They are also the only solution against residual emissions that cannot be eliminated, which are estimated to account for around 20% of current emissions.

A distinct engagement approach for climate issues

At Allianz Global Investors, we have a long-standing commitment to the stewardship of the companies in which we invest. Engagements on environmental topics, including climate change, accounted for one-fifth of our engagement activities in 2020 and continue to increase.

One of our priorities is to ensure that the data companies report aligns with “real” net-zero progression. In other words, we want to see that their efforts are contributing to a genuine decarbonisation of portfolios. Building on our own net-zero goals3 – and those of our parent company, Allianz4 – we have enhanced our climate-related engagement strategy. Some key factors underpinning our process include:

- We use existing and evolving data sets to assess individual firms’ climate strategies, policies, initiatives and performance relative to peers. This helps us refine our engagement approach relating to specific elements of each company’s transition pathway.

- We seek a robust understanding of how they calculate their targets and examine which of their business practices are covered.

- We look for firms to align with best practices within their peer groups, for example in those sectors where non-CO2 greenhouse gases are a more pressing factor (eg, methane for utilities). In these instances we will engage specifically on these details. We also consider factors beyond environmental issues to ensure social and governance related aspects are appropriately integrated into companies’ climate strategies.

- We have a particular focus on “just transition” as we seek to ensure that environmental goals do not have detrimental social impacts. This can involve understanding the impact of an ambitious climate transition strategy on the workforce, local communities and other stakeholders.

- We introduce binding goals, which are reviewed and tracked over a period of several years. Our approach to “co-investing” in climate transition favours engagement over exclusion or divestment.

Consistency is key

As the flagship goal of the Paris Agreement, net zero is a powerful concept – but the reality of achieving it is complex. A robust framework to measure and scope out investee companies’ climate factors, supported by a rigorous, ongoing engagement process, is critical in directing capital towards achieving shared climate goals.

We hope the unprecedented surge in pledges to achieve net zero will continue. They should be complemented by greater consistency and agreement on how we collectively define net zero, which should in turn help further drive mobilisation on a global scale.

1 Global Warming of 1.5°C report by IPCC (Oct 2018) https://www.ipcc.ch/site/assets/uploads/sites/2/2019/06/SR15_Headline-statements.pdf

2 https://racetozero.unfccc.int/wp-content/uploads/2021/04/Race-to-Zero-EPRG-Criteria-Interpretation-Guide-2.pdf

3 https://www.netzeroassetmanagers.org/

4 https://www.allianz.co.uk/about-allianz/environmental-responsibility/net-zero-asset-owner-alliance.html

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication’s sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP (Australian Registered Body Number 160 464 200) is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

1824158 | COMM-431 | 5844