Summary

The best way for investors to ensure that oil majors become enablers of the global transition to net zero by 2050 could be through concerted engagement. The world must urgently expand its clean energy sources, and we believe divestment would do little to achieve this goal.

Key takeaways

|

The relationship between energy and climate change is complex

Energy powers progress and is essential to deliver economic development and fundamental human rights: nearly 1 billion people worldwide still do not have access to power simply for cooking and heating. However, population growth and rising economic output are driving up greenhouse gas (GHG) emissions, most of which are caused by burning fossil fuels to meet energy needs. It is therefore vital not only to tackle climate change (UN Sustainable Development Goal 13), but also to ensure access to affordable, reliable and sustainable energy (UN SDG 7).

The IEA’s pathway to net-zero emissions

In May 2021, the International Energy Agency (IEA) published its pathway to reach net-zero emissions by 2050. While it is one pathway, rather than the only pathway, this plan is an official IEA blueprint, and as such it has inherent credibility. It will be used by many investors to align their portfolios to a net-zero trajectory and will inform corporations’ plans to reach net zero. The IEA’s document sets out an ambitious and radical blueprint. According to Dr Fatih Birol, IEA executive director, it highlights the “gap between rhetoric and real life”. Without the clear picture of the challenge that the IEA presents, we could end up in a place where companies and portfolios are decarbonising, but the real economy isn’t.

Under the IEA net-zero pathway, the global energy system will look completely different by 2050. Global energy demand will be around 8% lower than today, but that energy will power a global economy more than twice as large, with a population 2 billion greater.

- Almost 90% of electricity will be supplied by renewable energy sources (almost 70% of that figure will come from wind and solar; nuclear power will supply much of the rest).

- The largest source of energy in the world will be solar power (approximately 20% of supply, up from 1% today).

- Oil and gas consumption will decline by 75% and 55%, respectively, by 2050.

- There will be no need for new oil and gas supplies, and the remaining demand will be met by low-cost producers. The market share of OPEC (Organisation of the Petroleum Exporting Countries) nations will climb to 52%, from 37% currently.

- All remaining coal-fired power plants will use technologies that remove harmful emissions.

Overall, the IEA has identified more than 400 milestones to help governments meet their target of keeping global warming within 1.5°C of pre-industrial levels.

Divestment will not decarbonise the economy

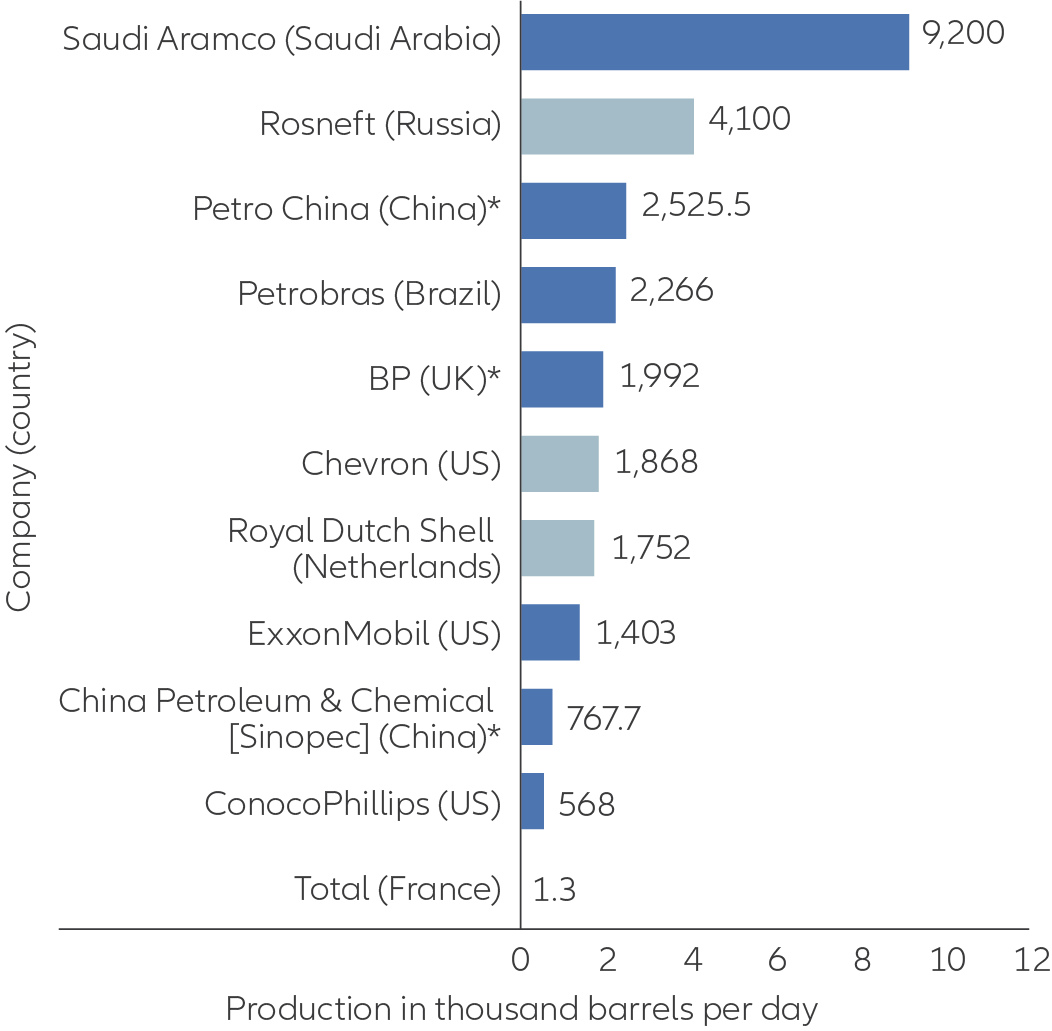

Divestment will do little to address climate change. It will simply displace the problem. If responsible, active investors divest, potentially less responsible investors (or those that are less exposed to reputational and regulatory pressures) will replace them and continue to fund “business-as-usual” strategies. Oil and gas majors account for just 12% of global reserves, 15% of production and 10% of estimated emissions from industry operations. The winners from divestment would be state-owned enterprises and national oil companies, which own the bulk of reserves. The benefit in climate terms is unclear.

Given the importance of fossil-fuel revenues to their economic growth and social stability, it is debatable whether petrostates will “strand” their reserves to curb global warming. The IEA pathway suggests that OPEC and other oil-exporting countries will see their governments’ hydrocarbon revenues collapse by 75%.

State-owned and national companies led oil production in 2020

1,000 barrels of oil per day

Source: Statistica. Most recent available data as at 7 June 2021.

It is equally important to influence the pattern of energy demand. More than half the cumulative shift to green energy consumption envisaged in the IEA net-zero pathway is linked to consumer choices. Governments must therefore provide the regulatory and policy frameworks within which companies will formulate their business plans and consumers will change their habits.

We need an orderly energy transition supported by current and emerging technologies. Global action on energy efficiency is essential. This critical area can deliver big reductions in emissions while supporting economic growth, reducing air pollution and saving consumers money. Renewables have a major role in combination with natural gas (viewed as a transitional fuel for power generation since it generates half the GHG emissions of coal) and further supported by battery storage.

Green hydrogen is a credible option, although it needs demand at greater scale to become economically viable. Sustainable biofuels can provide a substitute for conventional fuels. Carbon capture, usage and storage (CCUS) is often promoted by the oil and gas industry, as well as energy-intensive sectors such as steel and cement, to reduce GHG emissions. However, CCUS currently lacks political support and social acceptance and requires a pricing signal in the form of a global carbon tax. Nature-based solutions such as reforestation and wetlands can help to avoid, reduce and offset emissions, provided they are independently verified.

Oil majors have important skills that can support the transition

The IEA also recognises that oil majors have a role to play in making its roadmap a reality.1 They have the global reach, large-scale project management capabilities, government relationships and commercial expertise to manage volatility along integrated energy value chains. European oil majors are competing successfully in renewable energy auctions in partnership with specialist infrastructure investors and adopting ambitious medium and long-term capacity targets. That said, oil majors are generally perceived as being part of the problem.

Climate change and finite supplies of scarce resources are two sides of the same coin – and interlinked

We believe it is important to take a nuanced approach that considers and compares GHG emissions from all energy sources across their full lifecycle. Renewable energy is intermittent by nature and must be offset by nuclear (decarbonised but controversial), natural gas or – in the worst case – coal. Manufacturing solar panels and wind turbines is carbon-intensive and major questions remain over their decommissioning and recycling. Depletion of natural resources must be carefully monitored, particularly the rare-earth minerals required to make solar panels and batteries. The IEA estimates that annual demand for critical minerals will increase from around 7 million tonnes in 2020 to 42 million tonnes by 2050. It admits that this demand will be much more concentrated as deposits of rare-earth minerals are more geographically focused than fossil fuels. These concentration issues create supply challenges that will need to be addressed.

Oil majors must demonstrate their commitment to net zero

If we are to believe that oil majors can play a constructive role in the energy transition, they must provide evidence of their commitment to a low-carbon transition, such as:

- Endorsing the recommendations of the Taskforce on Climate-Related Financial Disclosures

- Reporting more consistently on climate-related risks

- Joining the Science-Based Targets initiative and working on the oil and gas decarbonisation framework

- Committing to reach net zero by 2050 as well as setting interim targets

- Reporting transparently and credibly on progress in reducing Scope 1 and 2 carbon emissions as well as on the most material Scope 3 emissions

- Addressing methane emissions as a first step to protecting the green credentials of natural gas

- Monitoring their lobbying activities to ensure that these do not contradict their commitment to a low-carbon transition

- Building out their new energy businesses

In the future, we plan to invite oil majors to put their climate action plans to a shareholder vote. Transparency in this area is critical if investors are to hold them to account on their decarbonisation strategy. How we vote ourselves will depend on the progress of our engagement with the boards. Engagement at the corporate level is essential. But by active stewardship we also mean engagement at the policy level, both individually and collectively.

1IEA World Energy Outlook, January 2020, p160 onwards

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP (Australian Registered Body Number 160 464 200) is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

1874149