US banks: five factors to watch after First Republic’s collapse

Three high-profile bank failures in two months have prompted investors to scrutinise the robustness of the overall US banking sector. In our view, the recent rescue of First Republic Bank should help allay the risk of contagion. But as other banks make the headlines, there might still be stress ahead – and we identify five factors to monitor in the months ahead, including a heightened risk of digital bank runs.

Key takeaways:

- The latest strains affecting US regional banks have intensified the spotlight on the health of the country’s banking sector.

- From the effects of lending headwinds to the scale of credit losses, we think there are five factors investors may watch for signs of further pressure.

- The stress has also highlighted how, in a digital age, guarding against the risk of bank runs is becoming increasingly difficult.

What has happened?

First Republic Bank was another recent casualty of stresses in the US banking sector following the collapse of Silicon Valley Bank (SVB) and Signature Bank in March. After disclosing more than USD 100 billion in underlying outflows in the first quarter1, First Republic saw regulators step in and facilitate a sale of its assets to JP Morgan Chase & Co.2 It is the largest US bank failure since the 2008 financial crisis. In the days since the rescue, the shares of some other US regional banks have fallen.3

What does the future hold for the sector?

Our view

We think the sale of First Republic assets to JP Morgan should reduce the risk of a broader crisis in the US banking sector. Speaking after the deal was announced, JP Morgan chief executive Jamie Dimon sought to allay fears of further bank failures.4 As he noted, relatively few US banks – other than First Republic and SVB – had both very large uninsured deposit bases and significant long-duration fixed rate assets which had lost value due to the rapid increase in US interest rates. The takeover of First Republic may not mark the end of the current panic, as some of the remaining 4,500 US banks may still need additional help, and other names in the sector have subsequently come under the spotlight. But it hopefully marks the beginning of the end of concerns about the health of large US banks.

Still, we think there are five areas to monitor across the broader US banking system in the coming months amid stresses that stem from a higher interest rate environment.

Five areas to monitor across the US banking system

- Effects of lending headwinds:

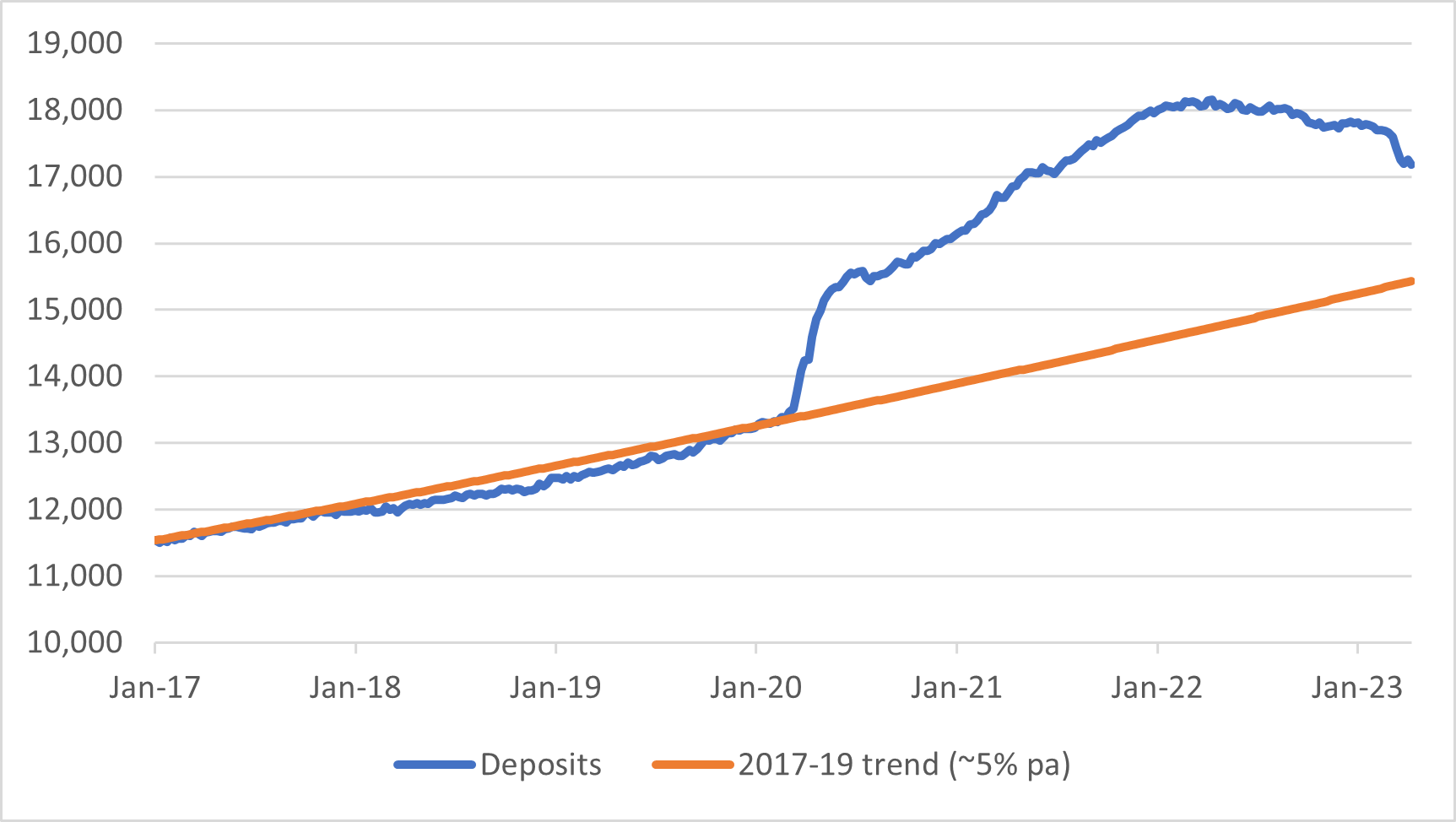

Banks’ business models rely on taking in deposits and giving out loans. As a consequence of the aggressive cycle of interest rate increases by the US Federal Reserve, cash now has a value again, and many depositors want to earn the higher rates being offered by treasuries, money market funds, and other non-bank products. At the same time, quantitative tightening is acting to drain deposits from the banking system (see Exhibit 1). As a result of these factors, banks have had to pay more to secure deposits, driving their profit margins down and limiting their appetite to make loans. This potential reduction in profit margins has led to fears that last year was “as good as it gets” for US banks. From a wider perspective, the resulting tighter availability of credit could also impact the broader economy and limit the ability of firms and households to make investments.

Exhibit 1: Total deposits of US banks (USD billion)

Source: Deposits, all commercial banks. Data from Board of Governors of the Federal Reserve System. Sourced from Federal Reserve Bank of St. Louis. Data as at 2 May 2023.

- Scale of credit losses:

Defaults on bank loans – otherwise known as credit losses – have begun to creep up in recent quarters. During Covid-19, credit losses fell to historically low levels, supported by large fiscal stimulus in the initial phases of the pandemic, and then remained low as the economy re-opened, helped by low unemployment, strong wage growth, and pent-up savings from the Covid-19 era. But they are now rising, most notably in areas that can act as leading indicators of borrower stress, such as subprime car loans and credit cards. The key question is how much further will credit losses increase? - Depth of real estate stress:

Offices represent around a quarter of total commercial real estate debt held in the US banking system. Declining office values due to increasing working-from-home and higher interest rates may cause stress for those banks that have built up large exposure to this sector relative to their size. We think credit losses for the banking system as a whole are manageable. But while the largest banks have limited exposure, some smaller banks who have been aggressive lenders to the sector may struggle in the coming years as they work through this credit cycle. - Size of unrealised losses:

As interest rates have risen, the market value of many of the securities banks hold has fallen. Similarly, the fair value of many of their loans with fixed interest rates have declined. Many banks haven’t recognised the fair value – or mark to market – impairments in their accounts, raising some concerns about the impact on capital if these risks are realised. We don’t see this as an issue facing all banks uniformly, but it is an area that might affect some smaller regional banks. - Risk of digital bank runs:

In a digital age, guarding against the risk of bank runs is becoming increasingly difficult. Depositors can move their cash between accounts instantly and from anywhere, while social media can allow concerns or rumours to spread quickly. Regulators and banks will need to manage the challenge of depositors potentially more prone to moving their cash.

Three bank failures in two months have shaken investor confidence in a sector key to the health of the broader economy. Overall, we think US banks face a challenging remainder of 2023. Profitability has probably peaked, compounded by a likely slowdown in loan growth and a rise in credit costs.

In the wake of these bank failures, regulators are likely to enforce stricter regulation, including requiring banks to hold more capital and subjecting a larger number of banks to more rigorous stress tests, that will further pressure returns. The swift actions of regulators have helped to reduce the risk of a broader crisis, and JP Morgan’s rescue of First Republic hopefully marks the end, or at least the beginning of the end, of this phase of the crisis.

But US depositors and investors are more nervous about the safety of banks than they have been in more than a decade. Investors can use the factors above as a guide for potential signals of future stress.

1 Source: FRB Earnings Release Q1 2023 (firstrepublic.com). Excludes $30bn deposit made by consortium of other banks during March 2023.

2 Source: FDIC: PR-34-2023 5/1/2023

3 Source: Jamie Dimon to investors: ‘This part of the crisis is over’ | Fortune

4 Source: Jamie Dimon to investors: ‘This part of the crisis is over’ | Fortune