The China Briefing

What can trigger a recovery in confidence?

China A-shares are up 10% post Chinese New Year in early February, and China H-shares are up more than 25%

Please find below our latest thoughts on China:

- Just past the halfway stage of the year, returns from China equities have not been spectacular. Offshore markets have at least registered positive returns with the MSCI China Index up 7%, while China A-shares are modestly lower.1

- The overall figures do, however, camouflage the market recovery from the sharp sell-down at the beginning of the year. China A-shares are up 10% post Chinese New Year in early February, and China H-shares are up more than 25%.2

- Looking ahead, for China A-shares in particular, one of the keys to a more sustained market recovery will be getting domestic households back into the stock market.

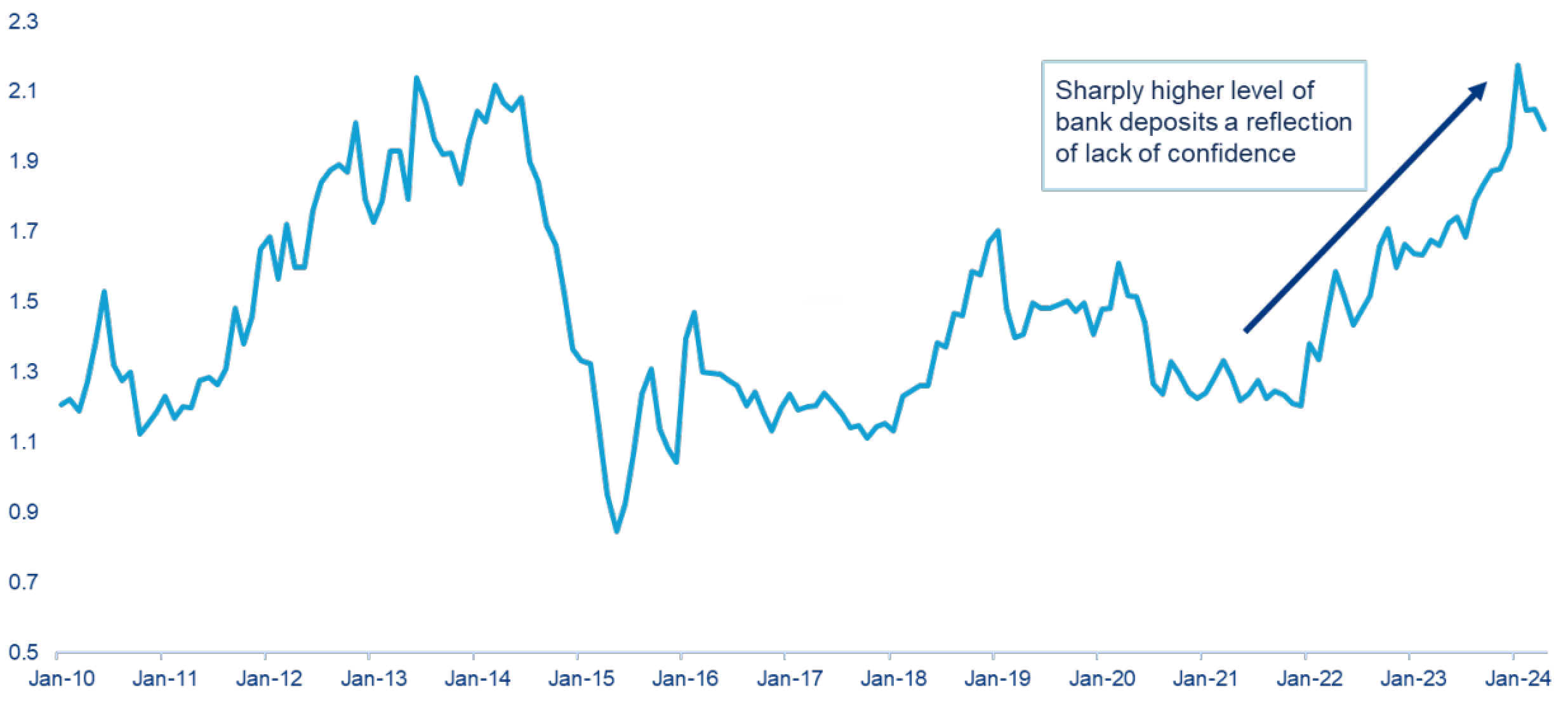

Chart 1: Household bank deposits as proportion of China A-Share market capitalisation

Source: Wind, HSBC as at 30 April 2024

- Animal spirits remain quite depressed locally. There are a number of ways to assess this – the lower level of overall market volumes, the subdued level of buying equities on margin, and how bank deposits continue to rise.

- Indeed, household bank deposits have now reached around twice the size of the overall China A market.3

- While this is an explanation of the extended market doldrums, it’s also a reminder that even small improvements in domestic confidence can have a significant impact when cash is deployed back into the stock market.

- A key question, therefore, is what could be the catalyst to trigger a recovery in confidence?

- In our view, ultimately the answer is a more convincing and durable economic recovery leading to an improvement in corporate earnings. And as the biggest drag on the economy is the continuing property downturn, then this is also the area which provides some likely clues for the equity market outlook.

- One of the big challenges in stabilising the housing market is the presales system – until potential homebuyers are confident that property developers are not heading for financial collapse, they are very unlikely to commit funds to new home purchases even at lower prices.

- This was reflected clearly in June property data when the average year-on-year sales growth of state-owned enterprises – viewed as having stronger balance sheets – finally turned positive after 12 months of negative figures, while private enterprise property sales remain firmly in the doldrums.4

Chart 2: Centaline Asking Price Index - China tier 1 cities

Source: Wind, Centaline as at 1 July 2024, using 1 month moving average

- Other recent high-frequency data points also show some pick-up in the secondary market in China’s largest cities. Average daily transaction volume in Shanghai in June, for example, was the highest since April 2021.5

- And the Centaline Asking Price Index in Tier 1 Cities, which include Beijing, Shanghai, Guangzhou and Shenzhen, has picked up from its low point in April this year.6

- This index reflects a forward-looking view of homeowners on the price at which they can sell their property units. A rising index therefore reflects some improvement in bargaining power and as such can be seen as a leading indicator for the secondary home price trend.

- Whether these recent improvements can be sustained over the summer period, in what is typically a lull period for property, is still to be seen.

- And more broadly, it is clear that while there has been an important pivot in property policy in recent months, more is certainly needed.

- Which brings us to an important second point about what can restore domestic investor confidence in China – more consistent policymaking.

- Indeed, July will be a busy month for China policy watchers. The so-called Third Plenum is scheduled for 15-18 July, followed by the more economically focused Politburo meeting, which is usually convened at the end of the month.

- While there are likely to be a lot of media headlines about the Third Plenum – it was made famous in 1978 when Deng Xiaoping announced the “open door” policy on foreign trade – in practice we think this is unlikely to have a major impact on equity markets.

- The Third Plenum is typically about big picture setting and ideology. So the focus will most likely be on reinforcing the existing direction of strategic travel such as the development of technological and innovation capabilities, and potentially some reforms of the fiscal and tax system.

- There are, in our view, unlikely to be updates on near-term economic policy, especially as it relates to the property sector. For these we will need to wait until the next Politburo meeting in a few weeks’ time.

1 Source: Bloomberg as at 3 July 2024

2 Source: Bloomberg as at 3 July 2024

3 Source: Wind as at 30 June 2024

4 Source: JP Morgan as at 2 July 2024

5 Source: HSBC as at 4 July 2024

6 Source: HSBC as at 4 July 2024