Active is: Sharing insights

3 ideas for investors seeking diversification and growth potential

Summary

After months of strong outperformance, US markets may face new challenges, including a resurgent coronavirus and political uncertainty. Our US Investment Strategist has three ideas for investors seeking diversification and growth potential: sustainable investing, private-market debt, and securities in Asia and Europe.

Key takeaways

|

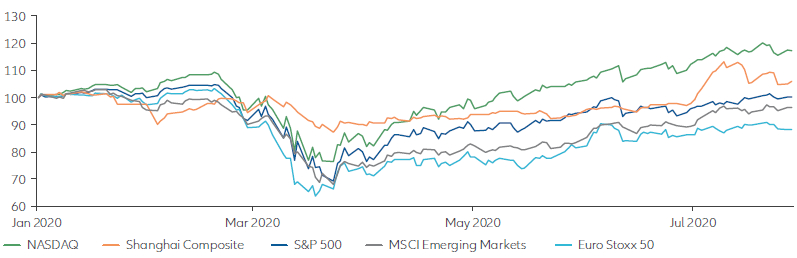

The coronavirus pandemic has taken equity and fixed-income investors on a roller-coaster ride this year – first with a remarkably rapid downturn, and then with a pronounced rebound. But the US stockmarket rally since the lows of 23 March has been largely concentrated in a few sectors, including those that benefited from a boom in remote work (particularly US large-cap tech stocks), defensive assets (including US investment-grade bonds and gold) and, to some extent, equities in China (see Chart 1).

Chart 1: the NASDAQ and China’s equity markets have outperformed most global indices this year

Global equity index performance (year to date; indexed to 100)

Source: Bloomberg. Data as at 28 July 2020. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any Allianz Global Investors product.

Heading into the final quarters of the year, investors in US markets face several potential headwinds. Large-cap tech stocks and the tech-heavy NASDAQ moved up more than 15% between January and July and may experience more volatility in the near future. In addition, the reopening of the US economy was expected to support cyclical stocks, but this rally hasn’t occurred yet. It may not happen until a viable coronavirus vaccine is available, or until the healthcare outlook in the US and emerging markets improves.

Meanwhile, investors overall – particularly those seeking income – are also facing extended periods of historically low rates globally. Plus, market uncertainty and volatility has historically risen before the US presidential election – particularly in the weeks prior to election day. And many investors still hold elevated levels of cash on the sidelines, earning zero or even negative yields.

Against this backdrop, where can investors turn if they are looking for alternatives to traditional US equities and bonds? Here are three ideas that could offer investors portfolio diversification, stability and yield potential – and importantly, appear to be set up for future growth.

1276856

Want to view more?

Summary

With its successful containment of Covid-19, China’s ongoing recovery is likely to benefit its most closely connected neighbours.

-

Investing involves risk. The NASDAQ Composite Index is a market-value-weighted, technology-oriented index composed of approximately 5,000 domestic and foreign securities. The Standard & Poor’s 500 Composite Index (S&P 500) is an unmanaged index that is generally representative of the US stock market. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. The Shanghai Stock Exchange Composite Index is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The Euro Stoxx 50 Index provides a blue-chip representation of supersector leaders in the region and covers 50 stocks from 11 euro-zone countries. The MSCI USA ESG Leaders Index is a capitalization-weighted index that provides exposure to companies with high ESG performance relative to their sector peers. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index. China A-shares are the stock shares of mainland China-based companies that trade on the two Chinese stock exchanges: the Shanghai Stock Exchange and the Shenzhen Stock Exchange.

The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication's sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP (Australian Registered Body Number 160 464 200) is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

Sustainable investing is positioned well for the future

The crisis has renewed investor interest in sustainable investing – for example, by focusing on the environmental, social and governance (ESG) factors that can help determine companies’ resilience in challenging times. There’s also greater emphasis on how the recovery from the coronavirus crisis can be a “green” one, as countries seek to ensure that their long-term investments – particularly in infrastructure – also support sustainability goals.

Why sustainable investing now?

The ESG space has held up quite well during the market volatility we’ve seen this year (see Chart 2), perhaps because the coronavirus pandemic seems to have accelerated many ESG-related trends that were happening already. Companies and governments have noted that the shutdown created a large drop in carbon emissions around the world – prompting debate about how to turn this sudden shift into more lasting change. Sustainable investing is also now at the forefront of many policy and stimulus debates as well – including the recent announcement of Europe’s EUR 750 billion recovery fund (a coronavirus stimulus package focused on digitalisation and climate protection), and the policy proposals by US presidential candidate Joe Biden centred on clean energy. In today’s business environment, board diversity and executive compensation are also under scrutiny.

Chart 2: ESG investing has outperformed this year

MSCI USA ESG Leaders Index vs S&P 500 Index (year to date; indexed to 100)

Source: Bloomberg. Data as at 28 July 2020.

How to implement this idea: look for ESG-integrated strategies and/or impact strategies

Consider investing in strategies that focus on ESG factors not only as an additional layer of risk management, but for growth potential. Also consider sustainable strategies or “green bonds” as part of an allocation to impact investments. Impact strategies have a clear and quantifiable causal connection between the investment they make and the resulting impact. (Green bonds specifically raise funds dedicated to projects that have a positive environmental benefit.)

Private-market alternatives lend themselves well to long-term investors

While traditional portfolios can frequently follow a “60-40” equity-bond mix, we believe there is room for private-market alternatives – perhaps with allocations of 15% or more in the institutional space. While less liquid, these asset classes can offer the potential for stability, growth, high credit quality, and often outsized yields or returns to compensate for their illiquidity.

Examples include asset classes like private credit, and infrastructure debt and equity:

Chart 3: over the long term, infrastructure debt has low default rates

Cumulative default rates for corporates and infrastructure investments (%)

Source: Moody’s, “Infrastructure Default and Recovery Rates, 1983-2016”. Data as at July 2017.

Why now?

This year may be particularly compelling for private markets as an asset class, as traditional equity and fixed-income markets have rallied substantially from the March lows. In addition, a small number of sectors (including large-cap technology) are driving market returns, which could lead to elevated volatility for stocks. Private markets, on the other hand, are usually much less volatile and may lend themselves well to long-term investors. There may be other timely benefits as well:

How to implement this idea

Given these trends, one private-market strategy to consider is infrastructure debt. As noted above, this sector tends to have outsized exposure to growth areas like renewable energy. Infrastructure debt also offers enhanced yield potential and a stable credit profile that may be attractive to fixed-income investors looking to diversify. And as noted below, another private-market option for investors to consider is Asian private credit.

Look to Asia and Europe for interesting opportunities and valuations

US financial markets have been a focus area for many global investors through the pandemic, driven in part by high levels of liquidity, sound balance sheets, and outsized exposure to Covid-19 “winners” like technology and healthcare. However, for those investors who may want to diversify part of their US allocation, we would suggest considering other regions as well – particularly Asia and Europe.

Why now?

Increasing a portfolio’s non-US exposure could make sense now for several reasons. First, as coronavirus cases and hospitalisations in the US have surged, and the re-opening has paused to some extent, we see notably better health trends in areas like China and northern Asia broadly, as well as parts of Europe. This has helped these economies stabilise more quickly. These regions are also supported by a softer US dollar, which has weakened substantially through the crisis.

Second, from a sector perspective, parts of Asia tend to offer exposure to more growth areas like technology and communication services, while Europe generally offers more cyclical exposure, to sectors like financials, industrials and energy – both at more favourable valuations. As noted, Europe has also made substantial commitment to invest in areas like digitalisation and climate protection through its recently announced EUR 750 billion recovery fund. Overall, while markets in Asia and Europe have largely lagged the US so far this year, we see potential for global financial markets to play catch-up as we wrap up the second half of this year and head into 2021.

How to implement this idea

China and the north Asia region seem to be emerging from the coronavirus crisis favourably and are well-positioned for growth. Positive demographic trends in Asia are likely to be helpful for the healthcare, education and technology sectors – which may increasingly tap the Asian private credit market. More traditional investments for this region also include China A-shares in the equity space and Asian high yield in the fixed-income space.

European markets are also attractive. These are more established markets with higher exposure to cyclical sectors and can offer opportunities – in both equity and select high yield – at relatively favourable valuations, particularly as the reopening continues globally. Europe also has been a pioneer in ESG strategies and seems poised to grow its leadership, so we favour impact-investing strategies levered to this growth.