Summary

Recent market turbulence in China may have attracted attention, but the country’s transformation story is far from over. The Year of the Tiger could offer multiple opportunities for investors, notably around sectors related to China’s future technologies and climate programmes.

Key takeaways

|

This lunar new year, China is celebrating the Year of the Tiger – but this festive period arrives off the back of several notable episodes of economic turbulence and market volatility. The MSCI China index fell 21% during 2021 due to slowing consumption, high-profile issues within the property market and increased regulatory interventions.

At the same time, China has also committed to doubling its GDP by 2035 – a target that will require annual growth of 4.7%. The Covid-19 pandemic in China severely hampered economic growth initially – as it did worldwide – but China’s relative success in managing the coronavirus has helped its economy recover quickly.

If China is to meet its long-term economic goals, it will need a clear way forward. Fortunately for investors, China has been upfront about how it plans to achieve such an ambitious target with a strategy centred around tech-related industries and sustainability – two keys to investing during the Year of the Tiger.

The outlook for regulatory intervention

Government crackdowns in areas including China’s property sector and offshore listings fuelled the volatility economic weakness. Should investors fear further regulatory interventions as the year unfolds?

Onshore China equities may benefit from further US-China “decoupling”

At one stage during the sell-down in autumn 2021, the MSCI China Index was underperforming the S&P 500 by more than 40% over a six-month period, the worst relative performance in at least a decade. There have been signs of a stabilisation in the early days of 2022 but China equities have still meaningfully trailed the US.

But China equities do not all march in lockstep. There has been a marked divergence between China A-shares (which trade on the two main domestic Chinese exchanges) and offshore-dominated indices. In 2021, the MSCI China A Onshore Index returned 4.0%, compared to the offshore-dominated MSCI China Index’s return of -21.7%. In other words, during 2021, China A-shares outperformed by more than 25 percentage points.

These market shifts are happening against the backdrop of a broader US-China market “decoupling”. The Chinese government has clamped down on domestic companies listing on US exchanges. The restrictions announced were accompanied by a stricter cross-border security and already seem to have driven many overseas listings closer to home. During the second half of 2021 to early December, only one mainland China-based company priced a US IPO, against the 29 that listed in Hong Kong. As this process of separating the two countries’ markets continues, investors who want to understand the nuances between markets and identify opportunities will need on-the-ground insights.

Property concerns seem to have been managed

A rapidly cooling property sector was a central factor in stockmarket turbulence in 2021, with high-profile stocks in the sector – most notably China Evergrande – suffering dramatic falls. This came amid broader weakness in the property market. In November last year, 61 of 70 cities covered by the national home price survey saw declines in primary house prices. This sustained weakness prompted regulators to intervene in an attempt to ease the worst of the funding and liquidity crunch. The regulatory intervention served to amplify volatility last year, but it may help usher in a managed decline in property prices during the coming year rather than a crash.

Foreign interest in China appears relatively undimmed

While China undoubtedly faces several headwinds, these challenges do not seem to have diminished its appeal to foreign organisations. Research from HSBC in late 2021 suggested that, of more than 2,000 foreign-based companies operating in China, 97% plan to maintain their presence and 60% plan to expand their supply chains in China – or are already expanding.

Signs also suggest that Chinese policy changes have done little to stem venture capital investment. The shifting regulatory environment clearly demands attention from private equity investors trying to fund the next generation of leading Chinese companies, but the deal numbers suggest no slowdown in funding. According to research firm Prequin, venture capital investments in China during 2021 reached USD 130.6bn, a new record total and a 50% increase on 2020’s USD 86.7bn.

Expect China’s continued emergence on the world stage

The world’s eyes will be on China at the start of the new year with the Winter Olympics taking place in Beijing during February, and the country will be keen to present a positive image. Events in China during recent months demonstrate the need for investors to understand the broader political and social context within the country. A certain amount of volatility is part and parcel of investing in China, but a comprehensive grasp of the underlying environment can help investors navigate it.

China is entering “Phase 3”: here’s why it matters

We’ve written before about “Phase 3” of China’s emergence on the global stage, which could provide a platform for further opportunities for investors. (Phase 1 was when China joined the WTO and became as a major link in global supply chains, Phase 2 saw China overtake Japan as the second-largest economy and begin integration of its markets into the global financial system).

Phase 3 is arguably the toughest as China attempts to use its economic might to establish and cement its place at the top table while exercising its “soft” powers of diplomacy to build influence.

Sustainability is central to China’s ambitions

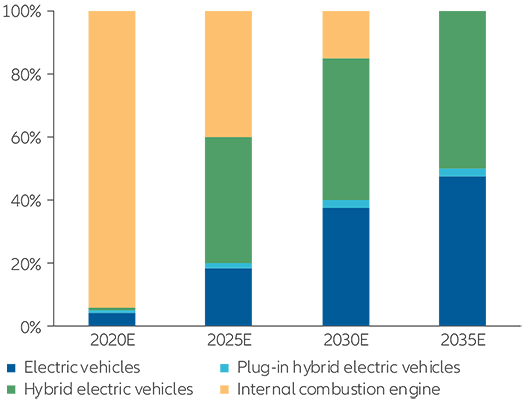

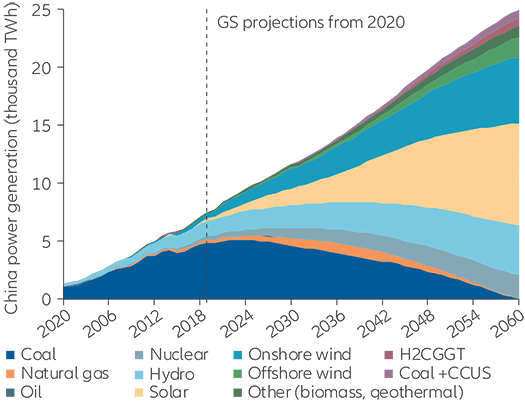

A key part of China’s transition lies in its determination to be seen to be taking a lead on climate change. The country has set out clear decarbonisation goals, and it used last year’s COP26 UN climate change conference as a platform to announce its willingness to co-operate with the US to achieve them. Before COP26, China had already committed to reach a peak in carbon emissions before 2030 and achieve net-zero carbon emissions by 2060. China is already the largest market for electric vehicles globally and, as Exhibit 1 shows, its reliance on EVs is expected to grow further. Similarly, government targets relating to energy provision (Exhibit 2) show a swing towards renewable sources before the 2060 deadline.

Exhibit 1: China passenger vehicle sales breakdown by

fuel type – government target penetration rates

Source: JP Morgan estimate.

Exhibit 2: China power generation breakdown

(thousand terrawatt hours)

Source: Goldman Sachs. Data as at January 2021.

There is still a long way to go, but if China continues its current trajectory, climate and sustainability could provide the ideal opportunity to write a positive new chapter in its history.

Expect continued focus on social issues

Beijing has been emphasising its goal of “common prosperity”, which it plans to achieve by tackling wealth inequality and ensuring the entire population feels a part of China’s growth story. We believe this is driven as much by a political agenda as an economic one, and it has caused some issues for investors. In an attempt to ensure fairer access to education, the government imposed a major clampdown on the private education sector, and there is ongoing pressure on generic drug prices to ensure they are affordable. Investors’ instinct may be to be wary of any further policies in the name of common prosperity, but the initiative could still create further investment opportunities, possibly linked to trends like healthier living and increased consumption.

Wealth inequality has been an issue in China for decades and, while it has not got significantly worse in recent years, it has attracted more public concern. The ruling Communist Party will want to be seen to be effectively tackling inequality in order to ensure legitimacy and popular support, especially as it approaches the 20th Party Congress in October, where President Xi Jinping will likely seek to be elected for a historic third term.

What it all means for investors

Here are four ideas for investors for the Year of the Tiger

- Seek out strategic sectors. Opportunities aligned with the topics above include sectors linked to China’s strategic need for self-sufficiency (semiconductors and robotics), and stocks linked to China’s carbon-emissions targets (renewable energy and the electric vehicle supply chain). Despite potential headwinds from the supply side (possible shortages of electricity and chips), we expect these sectors to continue to underpin China’s growth.

- Think “core” and “satellite” investments. One way to do this is by putting China A-shares at the core of a portfolio’s China allocation, and then adding thematic satellites focused on big-potential areas such as healthcare or future technologies. Themes relating to social trends like increased family sizes (incorporating branded baby clothes and food) and healthier lifestyles will also likely emerge.

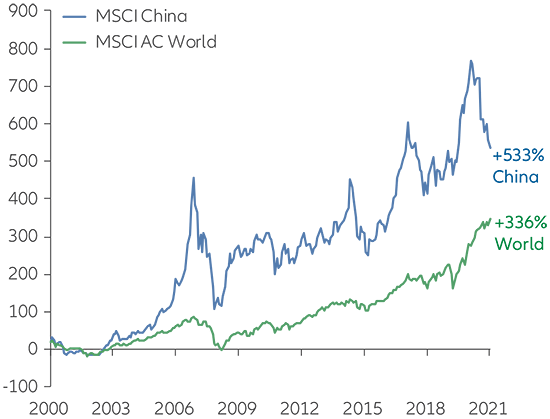

- Accept the reality of volatility. Investors would be well-served by accepting that volatility has historically accompanied China’s stockmarket growth (see Exhibit 3). An active approach may help investors navigate the shifting environment and to use the inevitable volatility to build positions.

- Learn how policy shapes the future. It is essential to understand China’s economic, social and cultural history – and how its policy agenda is evolving. This can help investors discover where the country’s strategic priorities translate into opportunities. Those sectors that are central to the country’s planned transformation should continue to enjoy political support and are consequently also less likely to be affected by regulatory change.

Exhibit 3: China equities have exhibited higher volatility – and attractive returns

MSCI China and MSCI ACWI performance since 2000 (in USD, indexed to 100)

Source: Bloomberg, Allianz Global Investors. Data as at December 2021. Based on net total return performance in USD. Past performance is not indicative of future results.

Index definitions

The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings.

The Standard and Poor’s 500 (S&P 500) is a stock market index tracking the performance of 500 large companies listed on stock exchanges in the United States.

The MSCI China A Onshore Index captures large and mid-cap representation across China securities listed on the Shanghai and Shenzhen exchanges.

The MSCI ACWI Index is designed to represent performance of large- and mid-cap stocks across 23 developed and 25 emerging markets.

Investing involves risk. TThe value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only. This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security.

The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believed to be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

This material has not been reviewed by any regulatory authorities. In mainland China, it is used only as supporting material to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document does not constitute a public offer by virtue of Act Number 26.831 of the Argentine Republic and General Resolution No. 622/2013 of the NSC. This communication’s sole purpose is to inform and does not under any circumstance constitute promotion or publicity of Allianz Global Investors products and/or services in Colombia or to Colombian residents pursuant to part 4 of Decree 2555 of 2010. This communication does not in any way aim to directly or indirectly initiate the purchase of a product or the provision of a service offered by Allianz Global Investors. Via reception of his document, each resident in Colombia acknowledges and accepts to have contacted Allianz Global Investors via their own initiative and that the communication under no circumstances does not arise from any promotional or marketing activities carried out by Allianz Global Investors. Colombian residents accept that accessing any type of social network page of Allianz Global Investors is done under their own responsibility and initiative and are aware that they may access specific information on the products and services of Allianz Global Investors. This communication is strictly private and confidential and may not be reproduced. This communication does not constitute a public offer of securities in Colombia pursuant to the public offer regulation set forth in Decree 2555 of 2010. This communication and the information provided herein should not be considered a solicitation or an offer by Allianz Global Investors or its affiliates to provide any financial products in Brazil, Panama, Peru, and Uruguay. In Australia, this material is presented by Allianz Global Investors Asia Pacific Limited (“AllianzGI AP”) and is intended for the use of investment consultants and other institutional/professional investors only, and is not directed to the public or individual retail investors. AllianzGI AP is not licensed to provide financial services to retail clients in Australia. AllianzGI AP (Australian Registered Body Number 160 464 200) is exempt from the requirement to hold an Australian Foreign Financial Service License under the Corporations Act 2001 (Cth) pursuant to ASIC Class Order (CO 03/1103) with respect to the provision of financial services to wholesale clients only. AllianzGI AP is licensed and regulated by Hong Kong Securities and Futures Commission under Hong Kong laws, which differ from Australian laws.

This document is being distributed by the following Allianz Global Investors companies: Allianz Global Investors U.S. LLC, an investment adviser registered with the U.S. Securities and Exchange Commission; Allianz Global Investors Distributors LLC, distributor registered with FINRA, is affiliated with Allianz Global Investors U.S. LLC; Allianz Global Investors GmbH, an investment company in Germany, authorized by the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin); Allianz Global Investors (Schweiz) AG; Allianz Global Investors Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; Allianz Global Investors Japan Co., Ltd., registered in Japan as a Financial Instruments Business Operator [Registered No. The Director of Kanto Local Finance Bureau (Financial Instruments Business Operator), No. 424, Member of Japan Investment Advisers Association and Investment Trust Association, Japan]; and Allianz Global Investors Taiwan Ltd., licensed by Financial Supervisory Commission in Taiwan.

1988389

Want to view more?

Summary

Disruption has always been around us, but we are moving to a new “survival of the fittest” digital era. We’ve identified key themes – from climate tech to AI – that are driving this new shift in a profound way, making disruption a critical factor for investors to build into their portfolios.

Key takeaways

|